Running a small business is not just about making sales. It is about managing timing. Bills arrive on fixed dates, payroll cannot wait, suppliers want payment upfront, and opportunities appear suddenly. Unfortunately, revenue rarely follows a predictable schedule. Even successful businesses regularly experience cash flow gaps.

This is why merchant financing has become one of the fastest-growing funding solutions for entrepreneurs. It provides quick access to working capital based on actual business performance rather than strict banking requirements. For many owners, it is the difference between missing a growth opportunity and capturing it.

This guide explains how merchant financing works, who it is for, how much it costs, and how it compares to other funding methods.

Why Cash Flow Is the Real Problem

Many business owners assume profitability determines survival. In reality, cash flow determines survival.

A company can show strong profits on paper but still fail if it cannot pay expenses on time. Consider a contractor who completes a $40,000 project but waits 60 days to get paid. During those two months, the business still must pay workers, buy materials, cover rent, and handle operating costs.

Small businesses face several common cash flow pressures:

- Seasonal sales fluctuations

- Slow-paying customers

- Inventory purchasing cycles

- Equipment repairs

- Payroll obligations

Traditional bank loans were historically the solution. However, banks evaluate tax returns, collateral, and credit history more than real-time revenue. Newer businesses or those with fluctuating income often do not qualify, even if they are healthy operations.

Merchant financing was created to solve this specific issue.

What Is Merchant Financing?

Merchant financing, often called a merchant cash advance, is a funding method where a business receives an upfront lump sum of money in exchange for a portion of its future sales revenue.

Instead of fixed monthly payments, repayment is collected as a percentage of daily or weekly sales. The financing provider purchases future receivables rather than issuing a conventional loan.

The key difference is simple:

A traditional loan is repaid on a schedule.

Merchant financing is repaid through business activity.

If the business has slower sales one week, payments are lower. If sales increase, repayment happens faster.

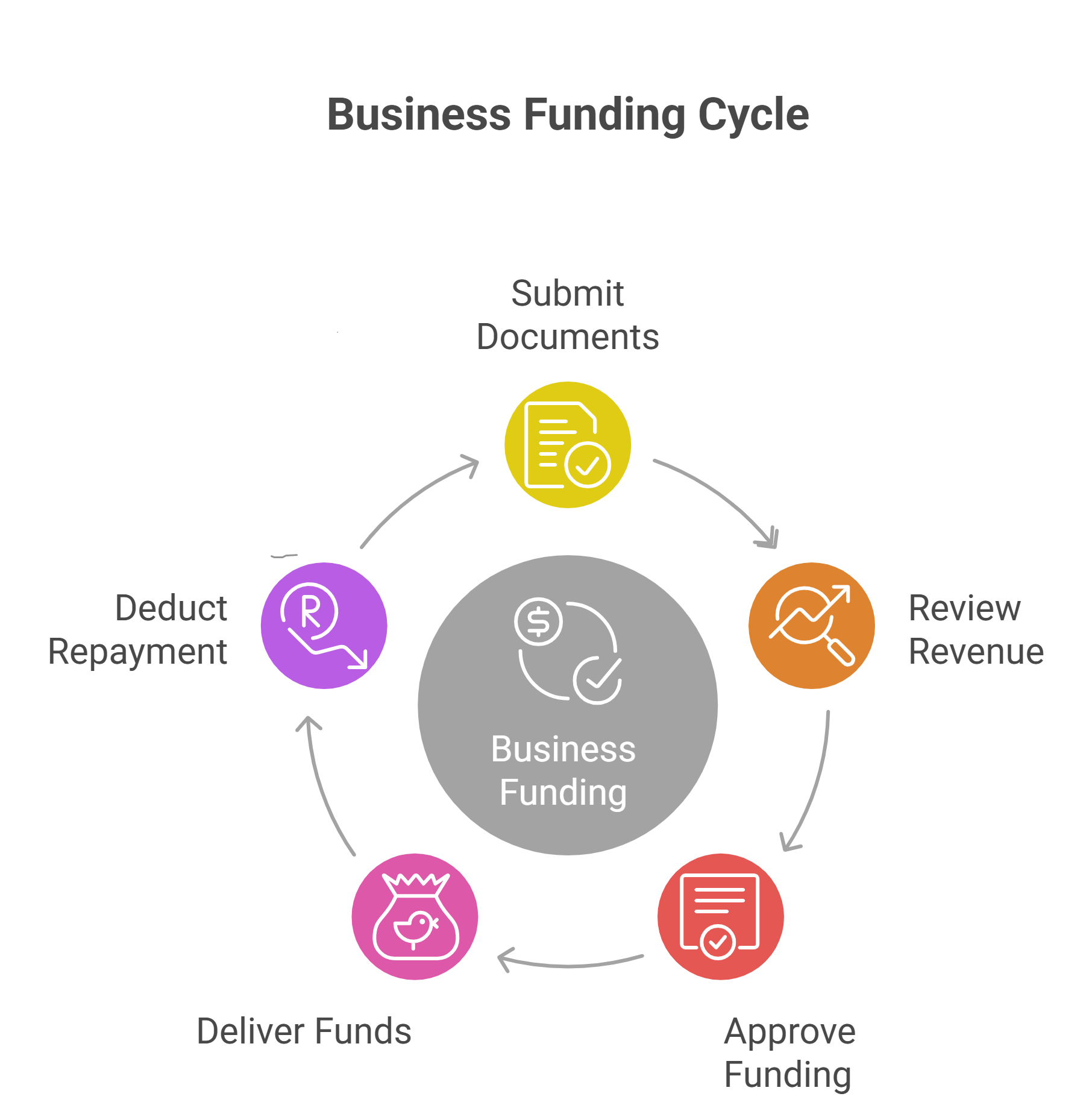

How the Process Works

The application process is much simpler than a bank loan.

- The business submits bank statements and sales history.

- The provider reviews revenue patterns.

- Approval is based primarily on consistent deposits.

- Funds are delivered quickly, often within a few days.

- A small percentage of daily or weekly revenue is automatically deducted until the agreed amount is repaid.

There is usually no requirement for real estate collateral or extensive financial statements.

Why Small Businesses Choose Merchant Financing

Speed

Funding can arrive in as little as 24 to 72 hours. Bank loans often take weeks.

Accessibility

Owners with lower credit scores can still qualify if revenue is steady.

Flexible Repayment

Payments adjust based on sales volume, reducing pressure during slow periods.

Simple Documentation

Most applications only require:

- 3 to 6 months of bank statements

- Business identification

- Basic operational information

For businesses facing urgent expenses, speed alone often makes merchant financing valuable.

Types of Merchant Financing

Merchant financing includes several related structures.

Merchant Cash Advance (MCA)

Repayment is collected from daily card transactions or bank deposits.

Revenue-Based Financing

Payments are calculated as a percentage of monthly revenue rather than daily sales.

Card Split Agreements

The payment processor automatically splits a portion of card sales to the funding provider.

All of these are built around the same concept: repayment tied directly to business performance.

Typical Costs and Fees

Merchant financing does not use traditional interest rates. Instead, providers charge a factor rate.

A factor rate typically ranges from 1.1 to 1.5. This determines the total repayment amount.

Example:

- Advance amount: $40,000

- Factor rate: 1.3

- Total repayment: $52,000

The repayment is fixed, but the time required to repay varies depending on sales volume.

Because repayment happens frequently and quickly, the effective annual cost can be higher than bank loans. This is why merchant financing is best viewed as short-term working capital rather than long-term debt.

Advantages of Merchant Financing

Fast access to capital

Owners can respond quickly to opportunities like bulk inventory discounts or seasonal demand.

No fixed monthly burden

Payments scale with revenue.

No major collateral requirement

Approval depends more on cash flow than assets.

Helpful for new businesses

Companies without long operating history can still qualify.

Risks to Consider

While useful, merchant financing must be used carefully.

Higher cost than traditional loans

The convenience comes with a premium.

Cash flow impact

Daily deductions reduce available operating cash.

Over-borrowing risk

Some businesses take multiple advances, creating repayment pressure.

Short repayment periods

Funds are typically repaid within 6 to 12 months.

Merchant financing works best when used to generate revenue, not to cover ongoing losses.

When Merchant Financing Is a Smart Choice

This funding works well when money will produce more money.

Good use cases include:

- Purchasing fast-selling inventory

- Emergency equipment repair

- Hiring staff before busy season

- Marketing campaigns

- Covering payroll during temporary gaps

Poor use cases include:

- Paying off long-term debt

- Covering chronic losses

- Expanding into new locations without proven demand

The goal should always be to increase revenue or efficiency.

How It Compares to Other Financing Options

Bank Loans

Traditional bank loans offer lower costs and longer terms. Many business owners still pursue small business loans usa because interest rates are significantly cheaper. However, qualification requirements, collateral demands, and long approval timelines make them impractical for urgent needs.

Receivable-Based Financing

Businesses that invoice customers often benefit more from working with an accounts receivable financing company. Instead of waiting 30 to 90 days for payment, outstanding invoices are converted into immediate working capital.

This option is common among wholesalers, distributors, trucking companies, and service providers.

Invoice Funding

Another alternative is invoice financing for small businesses. A lender advances a percentage of unpaid invoices, and repayment occurs once the customer pays. Costs are typically lower than merchant financing, and funding grows automatically with sales volume.

Who Qualifies?

Approval depends primarily on consistent revenue rather than credit score.

Typical requirements include:

- At least 6 months in business

- Regular bank deposits

- Stable monthly revenue

- Active business bank account

Businesses with $10,000 or more in monthly revenue generally have stronger approval chances.

How to Use Merchant Financing Responsibly

Before accepting funding, owners should evaluate how repayment affects daily operations.

Helpful tips:

- Calculate daily deduction amounts.

- Confirm the funding will generate new revenue.

- Avoid stacking multiple advances.

- Compare offers from multiple providers.

- Maintain a cash reserve whenever possible.

Merchant financing should support growth, not create dependency.

The Future of Merchant Financing

Digital underwriting, banking integrations, and financial technology platforms are rapidly transforming small business funding. Lenders can now analyze real-time bank activity, payment processing data, and revenue trends instead of relying only on credit reports.

As online commerce expands and traditional lending remains strict, revenue-based financing solutions will likely continue growing. Businesses increasingly prefer funding that moves at the same speed as their operations.

Final Thoughts

Merchant financing is not a perfect solution, but it is an important one. It fills a gap left by traditional lending institutions by providing fast, accessible working capital based on real business activity.

Used wisely, it can:

- Stabilize operations

- Fund growth opportunities

- Prevent cash flow disruptions

- Support seasonal expansion

The key is understanding its purpose. Merchant financing is a short-term financial tool designed to bridge gaps and capture opportunities. When paired with careful planning and responsible borrowing, it can help small businesses operate with confidence and agility in an unpredictable marketplace.