In today’s unpredictable business environment, companies face growing pressure to maintain stable cash flow while minimizing financial uncertainty. Rising operational costs, delayed customer payments, inflation, and market volatility have made financial risk management more important than ever.

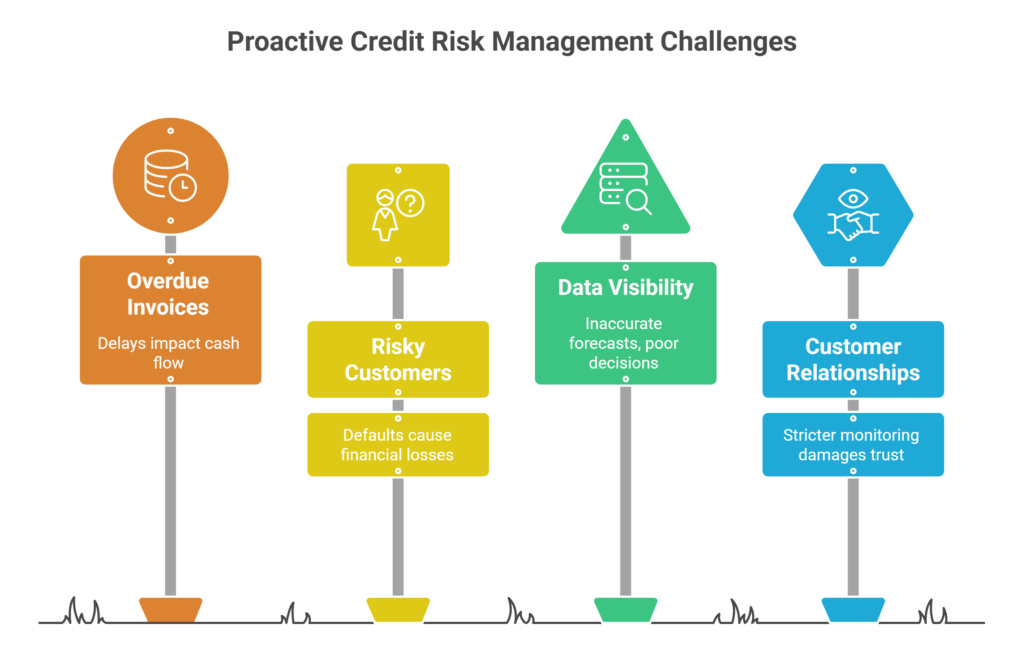

Businesses that extend credit to customers often struggle with late payments, unpaid invoices, and bad debt, all of which can disrupt daily operations and long-term growth plans.

This is why proactive credit risk management has become a critical strategy for businesses of all sizes. Instead of waiting for payment issues to occur, companies are now focusing on identifying risks early, monitoring customer payment behavior, and implementing preventive financial controls.

Businesses that adopt a proactive approach are better positioned to protect working capital, maintain healthy cash flow, and strengthen overall financial stability.

What Is Proactive Credit Risk Management?

Proactive credit risk management refers to the process of identifying, assessing, and reducing financial risks before they negatively impact a business. It involves continuous monitoring of customer creditworthiness, payment trends, and financial behavior to prevent bad debt and cash flow disruptions.

Traditionally, many businesses relied on reactive collections strategies. They would follow up only after invoices became overdue. However, this approach often results in:

- Cash flow shortages

- Higher bad debt losses

- Operational disruptions

- Increased financial stress

- Reduced business growth opportunities

A proactive strategy focuses on prevention rather than recovery.

Key Elements of Proactive Credit Management

Businesses implementing proactive credit management typically:

- Evaluate customer credit before approval

- Set clear payment terms

- Monitor customer financial health regularly

- Use automation to track receivables

- Detect payment risks early

- Improve collection efficiency

This approach helps businesses reduce uncertainty while improving long-term financial performance.

Major Factors Increasing Financial Risk for Businesses

The financial landscape has become increasingly challenging across industries. Companies are facing longer payment cycles, rising customer defaults, and increased pressure on working capital.

Economic Uncertainty and Market Volatility

Economic slowdowns and market instability have created financial pressure for businesses worldwide. Many companies delay vendor payments to preserve their own liquidity, creating a ripple effect across industries.

Rising Operational Expenses

Increased labor costs, transportation expenses, and supply chain disruptions are reducing business profit margins. As costs rise, businesses become more vulnerable to payment delays and financial instability.

Extended Credit Terms

To remain competitive, many companies offer longer payment terms to customers. While this may help attract new business, it also increases exposure to delayed payments and overdue receivables.

Growing Bad Debt Concerns

When customers fail to pay invoices, businesses absorb the financial loss directly. Excessive bad debt can severely impact profitability and operational continuity.

Because of these challenges, businesses are investing more heavily in financial risk reduction strategies and stronger receivables management systems.

Benefits of Proactive Credit Risk Management

Improved Cash Flow Stability

Cash flow is the foundation of every successful business. Even profitable companies can struggle financially if payments are delayed for extended periods.

Proactive credit risk management improves cash flow by:

- Reducing overdue invoices

- Improving payment collection timelines

- Identifying high-risk accounts early

- Increasing payment predictability

- Strengthening working capital management

Businesses with stable cash flow are better equipped to manage payroll, inventory purchases, expansion plans, and operational expenses.

Reduced Bad Debt Losses

One of the biggest advantages of proactive credit management is minimizing bad debt exposure.

By continuously monitoring customer payment behavior, businesses can:

- Reduce credit limits for risky customers

- Require partial upfront payments

- Adjust payment terms proactively

- Prevent excessive financial exposure

This helps businesses avoid major losses caused by customer defaults.

Better Financial Decision-Making

Modern businesses rely heavily on data-driven financial strategies. Proactive credit management provides better visibility into customer payment trends and receivables performance.

This enables companies to:

- Forecast cash flow more accurately

- Identify risky customer segments

- Improve budgeting and planning

- Make informed credit decisions

- Reduce uncertainty in financial operations

Better financial visibility leads to stronger business stability.

Stronger Customer Relationships

Many businesses mistakenly believe that stricter credit monitoring damages customer relationships. In reality, clear communication and professional payment processes often improve customer trust.

Businesses that establish transparent credit policies create:

- Better payment accountability

- Fewer invoice disputes

- Improved communication

- Long-term customer loyalty

Healthy customer relationships contribute significantly to long-term financial success.

Essential Components of Effective Credit Risk Management

Comprehensive Credit Assessments

Before extending credit, businesses should carefully evaluate customer financial stability.

Important Factors to Review

- Financial statements

- Credit history

- Industry reputation

- Existing liabilities

- Trade references

- Payment behavior

A thorough assessment process reduces the likelihood of onboarding high-risk customers.

Continuous Financial Monitoring

Customer financial conditions can change rapidly due to market conditions or internal operational issues.

Early Warning Signs Businesses Should Monitor

- Increasing payment delays

- Reduced order volumes

- Cash flow instability

- Frequent invoice disputes

- Communication gaps

Early detection allows businesses to take corrective action before problems escalate.

Clear Credit Policies and Payment Procedures

Strong credit policies create consistency and reduce financial confusion.

Credit Approval Standards

Businesses should establish clear qualification requirements before approving credit.

Defined Payment Terms

Clearly defined payment deadlines improve accountability and reduce misunderstandings.

Structured Collections Procedures

Businesses should maintain structured follow-up and escalation timelines for overdue invoices.

Appropriate Credit Limits

Setting appropriate credit limits helps minimize financial exposure.

Well-structured policies improve internal financial discipline and reduce operational risk.

Automation and Financial Technology

Technology is transforming the way businesses manage receivables and financial risk.

Benefits of Financial Automation Tools

Modern automation systems help businesses:

- Track invoice aging

- Send automated reminders

- Monitor payment trends

- Generate financial reports

- Improve collections efficiency

Businesses using automated financial systems often experience:

- Faster collections

- Reduced administrative workload

- Improved cash flow visibility

- Better financial forecasting

Automation improves both efficiency and financial accuracy.

Industry Trends Reshaping Credit Risk Management

AI and Predictive Analytics in Financial Risk Assessment

Artificial intelligence is becoming increasingly important in financial risk management.

Predictive analytics tools help businesses:

- Forecast payment delays

- Identify risky customers

- Detect financial warning signs

- Improve collection strategies

These technologies allow businesses to make faster and smarter financial decisions.

Increased Focus on Working Capital Optimization

Businesses are placing greater emphasis on maintaining liquidity and protecting working capital.

To improve financial flexibility, many companies partner with an Account Factoring Company that can provide faster access to cash tied up in unpaid invoices. This helps businesses maintain operational continuity without waiting for lengthy customer payment cycles.

Growing Demand for Alternative Financing Solutions

Traditional lending processes can sometimes be slow and restrictive, especially for growing businesses.

As a result, many organizations are now exploring Top Accounts Receivable Financing Companies to improve liquidity and maintain stable cash flow during periods of growth or economic uncertainty.

These financing solutions allow businesses to unlock working capital from outstanding invoices while reducing pressure on daily operations.

Later in the financial process, businesses experiencing temporary cash flow gaps may also consider Invoice Financing for Small Businesses as a flexible funding solution that supports operational stability without requiring traditional long-term debt.

Real-World Example of Proactive Credit Risk Management

Consider a wholesale distribution company that supplied products to multiple retailers using 60-day payment terms.

Initially, the business struggled with:

- Frequent late payments

- Cash flow shortages

- Delayed supplier payments

- Limited operational flexibility

Strategies Implemented by the Company

To improve financial stability, the company introduced several proactive measures:

- Monthly customer credit reviews

- Automated payment reminders

- Improved receivables tracking

- Risk-based credit limits

- Better communication between finance and sales teams

Results Achieved

Within one year, the company significantly reduced overdue invoices and improved overall cash flow predictability.

As a result, the business gained greater financial confidence and expanded operations more effectively.

Common Credit Risk Management Challenges

Despite its importance, many businesses still struggle with effective credit risk management.

Limited Financial Visibility

Without accurate reporting systems, businesses may fail to identify payment risks early.

Manual Processes

Manual invoicing and collections processes often create inefficiencies and delays.

Poor Internal Communication

Lack of coordination between departments can increase exposure to high-risk customers.

Resource Constraints

Smaller businesses often lack dedicated credit management teams or advanced financial tools.

However, even modest improvements in automation, monitoring, and communication can significantly reduce financial exposure.

Best Practices for Reducing Financial Risk

Businesses looking to improve financial stability should focus on several key strategies.

Regularly Review Customer Accounts

Ongoing customer evaluations help businesses identify financial risks before they become major problems.

Diversify Customer Portfolios

Avoiding overdependence on a small number of customers reduces concentration risk.

Use Data-Driven Financial Strategies

Financial analytics improve forecasting accuracy and strengthen decision-making.

Improve Internal Collaboration

Finance and sales teams should work together to balance revenue growth with financial protection.

Invest in Financial Technology

Modern financial systems improve efficiency, visibility, and collections performance.

Conclusion

Proactive credit risk management is essential for reducing financial risk and maintaining long-term business stability. In today’s uncertain economy, businesses cannot afford to rely solely on reactive collections processes.

By implementing preventive financial strategies, monitoring customer behavior continuously, leveraging automation, and maintaining clear credit policies, companies can improve cash flow, reduce bad debt exposure, and strengthen operational resilience.

Businesses that prioritize proactive credit management are better prepared to navigate economic challenges, protect working capital, and support sustainable long-term growth. As financial risks continue to evolve, proactive strategies will remain one of the most valuable tools for achieving business success and financial security.