Many business owners review their financial statements and feel confident when they see large figures listed under accounts receivable. Customers owe the company money, invoices have been sent, and sales were completed. It feels like the business has already earned that income.

However, accounting works differently from how most people naturally think about money. A company can report strong sales and still struggle to pay employees, suppliers, or operating expenses. The reason usually comes from misunderstanding one important concept. Revenue and collected cash are not the same thing.

Understanding how accounts receivable relates to revenue helps business owners manage cash flow, make better financial decisions, and avoid serious financial pressure even when sales appear healthy.

What Is Accounts Receivable?

Accounts receivable (A/R) is the money customers owe your business after you deliver goods or services but before payment is received.

When a business allows a customer to pay later, it is extending short term credit. Payment terms might be Net 15, Net 30, or Net 60 depending on the industry. Until the customer actually pays, the invoice amount is recorded as accounts receivable.

For example, a company completes a service worth $6,000 and sends an invoice requesting payment within 30 days. Until payment arrives, that $6,000 is listed as accounts receivable.

In accounting, accounts receivable is classified as a current asset because it represents a legal right to collect money in the near future.

Does Accounts Receivable Count as Revenue?

The clear answer is no.

Accounts receivable is not revenue. It represents unpaid revenue that has already been recognized.

Under accrual accounting, revenue is recorded when the business fulfills its obligation by delivering a product or completing a service. At that exact moment two entries occur:

- Revenue is recognized

- A receivable is created

Revenue measures what the company earned.

Accounts receivable measures whether the customer has paid yet.

When payment later arrives, the receivable is removed and replaced with cash. The business does not record new revenue at that point because the income was already recognized earlier.

Revenue vs Accounts Receivable

Many financial problems begin when business owners treat receivables like cash. The difference is important.

| Revenue | Accounts Receivable |

| Listed on income statement | Listed on balance sheet |

| Indicates business performance | Indicates unpaid invoices |

| Determines profitability | Determines collection status |

| Recorded when service is delivered | Exists until payment is collected |

Revenue answers the question: Did the business complete a sale?

Accounts receivable answers the question: Has the customer paid?

A business may show strong profits but still face financial stress if collections are slow.

Cash Accounting vs Accrual Accounting

The confusion often comes from two different accounting systems.

Cash Accountingaccounts receivable financing companies

Income is recorded only when money enters the bank account.

Accrual Accounting

Income is recorded when the service or product is delivered, even if payment comes later.

Most growing companies use accrual accounting because it reflects actual business activity. Lenders and investors also rely on it since it shows performance rather than payment timing.

Under this method, receivables appear whenever payment is delayed after a completed sale.

Why This Matters to Your Business

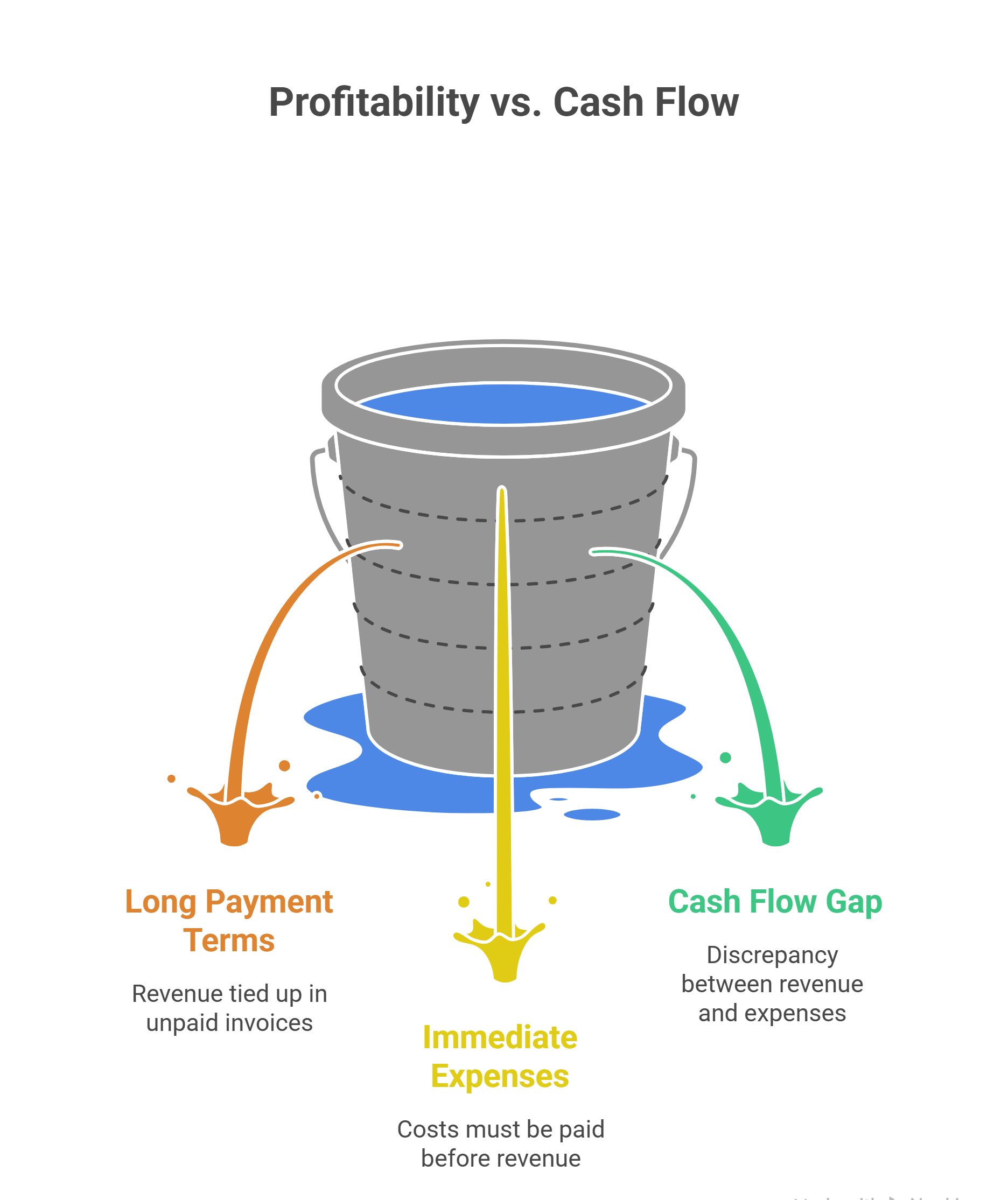

Profitability does not automatically mean stability. Many companies that show profit still experience cash shortages.

Consider a business that invoices customers on 60 day terms. If the company produces steady sales, a large portion of revenue could be tied up in unpaid invoices at any given time. Operating expenses still require immediate payment.

Common expenses include:

- payroll

- rent

- vendor payments

- utilities

- taxes

Because these costs must be paid before customers pay invoices, a company can face a serious cash flow gap even while profitable on paper.

The Impact of Late Payments

Late payments create financial risk. The longer an invoice remains unpaid, the harder it becomes to collect.

Businesses monitor this using an aging report:

- 0 to 30 days is normal

- 31 to 60 days indicates slower collection

- 61 to 90 days is concerning

- Over 90 days becomes high risk

If a customer never pays, the company must record bad debt expense and remove the receivable. The business originally recognized revenue but never received the money.

Converting Receivables Into Cash

When invoices accumulate and cash becomes tight, many businesses work with an accounts receivable financing company to improve liquidity.

Instead of waiting for customers to pay, the company receives funds based on outstanding invoices. The money can be used for payroll, inventory purchases, and daily operations. This keeps operations moving even when customers pay slowly.

Factoring and Immediate Liquidity

Another option involves working with accounts receivable factoring companies. In this arrangement, a business sells its invoices in exchange for immediate working capital.

Typical process:

- The business issues invoices

- The factoring provider verifies them

- The business receives a large advance

- The customer pays the factor

- Remaining funds are released after fees

Factoring does not increase revenue. It simply accelerates access to revenue that was already earned.

This is especially helpful for growing companies that have sales but need cash sooner.

Borrowing Against Business Assets

Some companies choose Asset based Lending as a financing strategy. This method allows businesses to borrow money using assets such as receivables, inventory, or equipment as collateral.

Instead of focusing only on credit score, lenders evaluate:

- invoice quality

- customer payment reliability

- concentration risk

- aging of receivables

Stronger receivables often mean stronger borrowing power.

How Accounts Receivable Appears in Financial Statements

Understanding where receivables appear helps clarify their role.

Income Statement

Shows revenue earned during the reporting period.

Balance Sheet

Lists accounts receivable as a current asset.

Cash Flow Statement

Shows whether recorded sales actually turned into cash.

If receivables increase, the company made sales but collected less cash. If receivables decrease, collections improved.

Financial professionals closely watch this because rapidly rising receivables can signal collection issues.

Real World Example

A wholesale distributor ships products to a retail store and issues a $12,000 invoice with 30 day payment terms. The distributor records the sale as revenue because the goods were delivered. At the same time the company records $12,000 as accounts receivable.

The distributor must still pay employees and suppliers while waiting for payment. When the retailer pays the invoice, the company does not record additional revenue. The receivable simply converts into cash because the earnings were already recognized.

Common Misunderstandings

Some owners believe receivables are guaranteed income. In reality they are expected collections, not certain collections.

Others assume higher revenue automatically means stronger finances. A company with slow paying customers may struggle more than a company with smaller but faster payments.

Another misconception is that profit ensures safety. In business, cash flow stability matters more than reported profit.

Tips for Managing Accounts Receivable

- Clearly state payment terms on invoices

- Send invoices immediately after completing work

- Track outstanding balances weekly

- Follow up before due dates

- Offer early payment discounts

- Review customer creditworthiness

Improving collections often strengthens cash flow faster than increasing sales.

Final Thoughts

Accounts receivable does not count as revenue. It represents revenue waiting to be collected.

Revenue shows performance.

Accounts receivable shows pending payments.

Cash shows usable money.

Many businesses experience financial pressure not because they lack customers but because funds remain tied up in unpaid invoices. Understanding this relationship helps you forecast cash flow, qualify for financing, and operate with confidence.

Once you clearly separate revenue from receivables, you begin managing your business based on financial reality rather than assumptions.