In today’s fast-moving business environment, access to capital can determine whether a company captures a growth opportunity or struggles to stay competitive. Many business owners seek quick funding to manage cash flow gaps, purchase inventory, expand operations, hire employees, or respond to unexpected expenses. However, obtaining fast financing is not just about filling out an application and waiting for approval. Lenders carefully evaluate several financial and operational factors before approving a quick business loan.

Whether you are a startup founder, a small business owner, or an established company looking for working capital, understanding the lender’s evaluation process can significantly improve your chances of approval. Businesses applying for a Startup Loan in USA often face stricter scrutiny because lenders must assess both business potential and repayment reliability.

This guide explores the key factors lenders review, common mistakes borrowers make, and practical steps businesses can take to secure faster approvals.

Why Quick Business Loans Have Become More Popular

Quick business loans have gained popularity because traditional lending processes can take weeks or even months. Modern businesses need faster access to funding to remain agile in competitive industries.

According to recent small business financing trends, many lenders now use digital underwriting systems to speed up approvals. Online lenders, fintech companies, and alternative financing providers have reduced processing times significantly, with some loans approved within 24 to 72 hours.

Businesses commonly use quick loans for:

- Managing short-term cash flow

- Purchasing inventory

- Covering payroll expenses

- Expanding operations

- Marketing campaigns

- Equipment upgrades

- Emergency repairs

However, speed does not eliminate risk for lenders. Even fast approvals require careful evaluation.

The First Thing Lenders Review: Business Credit Profile

Why Credit History Matters

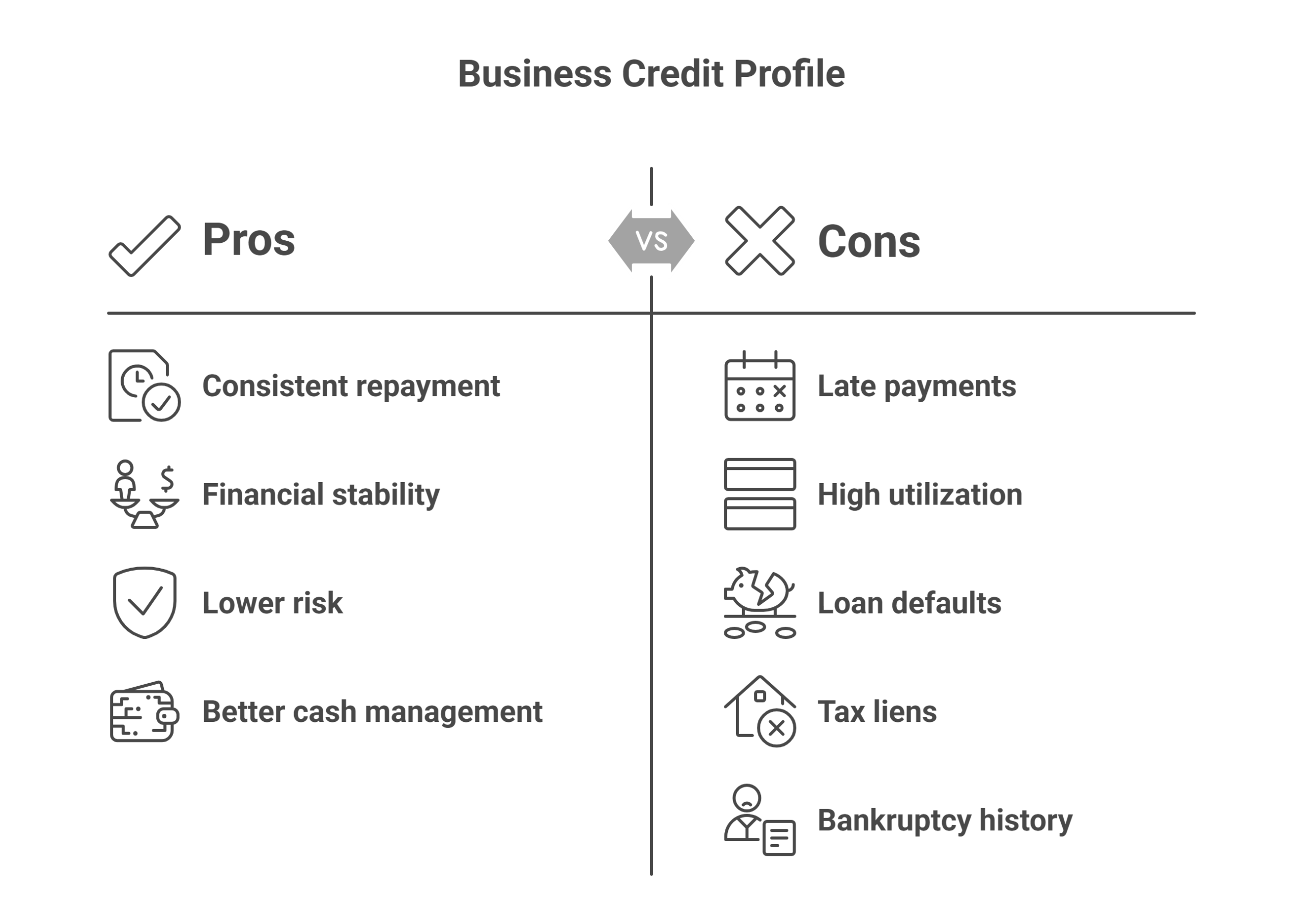

One of the most important factors lenders examine is your business credit profile. Credit history helps lenders determine how responsibly your company manages debt and financial obligations.

A strong credit score demonstrates:

- Consistent repayment behavior

- Financial stability

- Lower lending risk

- Better cash management

Lenders often evaluate both personal and business credit scores, especially for newer companies.

What Can Hurt Your Approval Chances

Common red flags include:

- Late payments

- High credit utilization

- Loan defaults

- Tax liens

- Bankruptcy history

- Excessive outstanding debt

For businesses seeking Small Business Loans in California, maintaining a healthy credit profile is especially important because competitive lending markets often create stricter qualification standards.

Revenue and Cash Flow Stability

Consistent Revenue Builds Confidence

Lenders want proof that your business generates enough income to repay the loan comfortably. Stable monthly revenue is often one of the strongest indicators of repayment capability.

Most lenders review:

- Bank statements

- Profit and loss reports

- Tax returns

- Accounts receivable

- Monthly sales trends

Businesses with unpredictable income may face higher interest rates or lower loan amounts.

Cash Flow Is More Important Than Profit Alone

A profitable business can still experience cash flow problems. Lenders focus heavily on liquidity because loan repayments require available cash, not just paper profits.

For example, a company waiting 60 to 90 days for customer payments may struggle to meet immediate obligations. In such cases, working with an Account Factoring Company can improve cash flow by converting unpaid invoices into immediate working capital.

This approach often strengthens a lender’s confidence because it demonstrates proactive financial management.

Time in Business and Industry Experience

Established Businesses Typically Receive Faster Approvals

Companies with longer operating histories generally pose less risk to lenders. Businesses operating successfully for several years have already demonstrated resilience, customer demand, and operational stability.

Many lenders prefer businesses with:

- At least 1–2 years of operations

- Consistent revenue history

- Proven customer base

- Industry experience

Startups Face Additional Evaluation

New businesses often lack extensive financial history. As a result, lenders place greater emphasis on:

- Business plans

- Founder experience

- Revenue projections

- Market demand

- Personal credit strength

Startups usually need stronger documentation and more detailed growth strategies compared to established businesses seeking financing.

Debt-to-Income and Existing Financial Obligations

Lenders Assess Overall Debt Burden

Before approving financing, lenders calculate how much existing debt your business already carries. Excessive debt reduces repayment flexibility and increases risk.

Key areas reviewed include:

- Existing business loans

- Credit card balances

- Equipment financing

- Merchant cash advances

- Vendor obligations

The Debt Service Coverage Ratio (DSCR)

Many lenders use DSCR (Debt Service Coverage Ratio) to determine whether a business earns enough income to cover debt payments.

A healthy DSCR typically indicates:

- Strong repayment ability

- Lower financial stress

- Better approval odds

Businesses with low DSCR ratios may need to reduce debt or improve revenue before applying.

Business Documentation and Financial Transparency

Organized Records Speed Up Approvals

Incomplete or inaccurate documentation is one of the most common reasons loan approvals get delayed.

Lenders usually request:

- Tax returns

- Bank statements

- Financial statements

- Business licenses

- Legal registrations

- Payroll records

- Accounts receivable reports

Businesses that maintain organized financial records often experience faster approvals and better loan terms.

Transparency Builds Trust

Lenders appreciate honesty regarding financial challenges. Attempting to hide declining sales, outstanding liabilities, or legal disputes can damage credibility and result in rejection.

Clear communication allows lenders to structure more realistic financing solutions.

Collateral and Asset Evaluation

Secured Loans Reduce Lender Risk

Some quick business loans require collateral. Assets help protect lenders if the borrower defaults.

Common collateral includes:

- Equipment

- Inventory

- Real estate

- Vehicles

- Outstanding invoices

Asset-backed financing has become increasingly common because it allows businesses to leverage existing resources for funding.

Alternative Financing Options

Companies lacking traditional collateral may explore:

- Invoice financing

- Revenue-based lending

- Purchase order financing

- Accounts receivable factoring

This financing method is especially useful for industries with long payment cycles, such as:

- Transportation

- Staffing

- Manufacturing

- Healthcare

Industry Risk and Market Conditions

Some Industries Are Viewed as Higher Risk

Lenders evaluate economic trends and industry-specific risks before approving loans.

Industries often considered higher risk include:

- Restaurants

- Construction

- Retail startups

- Seasonal businesses

- Hospitality

Factors influencing risk assessments include:

- Market volatility

- Economic downturns

- Customer demand fluctuations

- Supply chain disruptions

Businesses in Stable Industries May Receive Better Terms

Companies operating in healthcare, logistics, technology services, and professional consulting often receive more favorable lending consideration due to predictable demand and recurring revenue potential.

Digital Presence and Operational Credibility

Online Visibility Matters More Than Ever

Modern lenders increasingly review a company’s digital footprint during underwriting.

This may include:

- Business websites

- Online reviews

- Social media activity

- Google Business profiles

- Customer testimonials

A professional online presence helps validate operational legitimacy and customer engagement.

Real-World Example

Consider two businesses applying for identical funding amounts:

- Business A has updated financial records, positive online reviews, and a professional website.

- Business B has inconsistent branding, limited online visibility, and outdated records.

Even if both generate similar revenue, lenders may perceive Business A as lower risk and more reliable.

Common Reasons Quick Business Loans Get Denied

Many businesses fail to secure financing due to avoidable issues.

Frequent Denial Factors

- Poor credit history

- Inconsistent revenue

- Insufficient documentation

- Excessive debt

- Weak cash flow

- Limited time in business

- Unrealistic loan requests

Preparing thoroughly before applying can significantly improve approval outcomes.

How Businesses Can Improve Their Approval Chances

Strengthen Financial Management

Business owners should focus on:

- Paying bills on time

- Reducing unnecessary debt

- Monitoring cash flow regularly

- Maintaining accurate records

Improve Cash Flow Stability

Strategies include:

- Shortening customer payment cycles

- Negotiating vendor terms

- Building emergency reserves

- Using receivables financing solutions

Build Business Credit Early

Establishing trade lines and responsibly managing business credit accounts can strengthen future loan applications.

Apply for the Right Loan Amount

Requesting unrealistic funding amounts can trigger lender concerns. Businesses should calculate financing needs carefully and align requests with actual repayment capacity.

The Growing Role of Alternative Financing

Traditional bank lending standards remain strict, leading many businesses to explore alternative financing providers.

Today’s financing landscape includes:

- Online lenders

- Revenue-based financing

- Invoice factoring

- Asset-based lending

- Fintech funding platforms

This evolution has expanded funding opportunities for newer and underserved businesses.

Conclusion

Securing a quick business loan requires more than urgency it requires preparation, financial clarity, and operational credibility. Lenders carefully examine credit history, cash flow, revenue consistency, debt obligations, industry risk, and business documentation before approving funding.

Businesses that proactively strengthen their financial health, maintain organized records, and manage cash flow effectively stand a much better chance of receiving fast approvals with favorable terms.

Whether you are exploring traditional lending solutions or alternative financing options, understanding the lender’s perspective can help you position your business for long-term financial success.

Ready to Secure Fast Business Funding?

At State Financial, we help businesses access flexible financing solutions designed to improve cash flow, support growth, and simplify funding challenges. Our team is ready to help you find the right funding solution for your business goals.