Growth is the goal of every business, but growth without sufficient capital can quickly become a liability. Expanding sales, entering new markets, hiring talent, or increasing inventory all demand cash well before revenue is fully collected. Traditional financing options often struggle to keep pace with this reality. Fixed loan limits, rigid repayment schedules, and strict credit requirements can restrict a growing company just when flexibility matters most. This is where scalable financing solutions, particularly asset-backed structures, become essential.

One of the most effective tools for businesses navigating rapid growth is Asset-Based Lending (ABL). Designed to expand in line with operational performance, ABL provides access to working capital based on real, measurable assets rather than projections alone. Understanding how ABL works, who it benefits most, and how it compares to other financing methods can help business owners make smarter funding decisions.

The challenge of financing growth

According to small business finance studies, a significant percentage of growing companies experience cash flow gaps even while reporting strong sales. Late payments, longer receivable cycles, and upfront operating costs all contribute to liquidity pressure.Across many sectors, revenue is often locked in open invoices for extended periods, even though operating expenses such as wages, vendor payments, and fixed costs require constant and timely funding.

Traditional bank loans often fall short in these situations. Credit limits are typically fixed based on historical performance, and increases require lengthy reapproval processes. As a result, companies experiencing rapid growth may find themselves constrained by financing structures that were adequate at an earlier stage but no longer fit their operational reality.

What is Asset-Based Lending?

Asset-Based Lending is a form of commercial financing that allows businesses to borrow against the value of their assets. Rather than relying primarily on cash flow forecasts or personal guarantees, lenders evaluate tangible assets such as accounts receivable, inventory, equipment, and in some cases real estate.

The borrowing capacity under an ABL facility is determined by a borrowing base formula. As eligible assets increase, available credit increases as well. This structure makes ABL inherently scalable, aligning funding availability with business activity.

Unlike fixed-term loans, ABL facilities are typically revolving lines of credit. Funds can be drawn, repaid, and redrawn as needed, providing ongoing liquidity support rather than a one-time infusion of capital.

How ABL supports scalable growth

The primary advantage of ABL is its ability to grow alongside the business. When sales increase, receivables increase. When inventory expands to meet demand, collateral value rises. This dynamic relationship allows companies to fund growth without renegotiating financing terms every few months.

ABL is particularly effective for businesses that experience seasonality or uneven cash flow cycles. Manufacturers, distributors, wholesalers, and B2B service providers often use ABL to bridge the gap between production costs and customer payments.

Another key benefit is speed. Once an ABL facility is established, access to capital is driven by regular reporting rather than repeated underwriting. This allows management to respond quickly to opportunities such as bulk purchasing discounts, new contracts, or expansion initiatives.

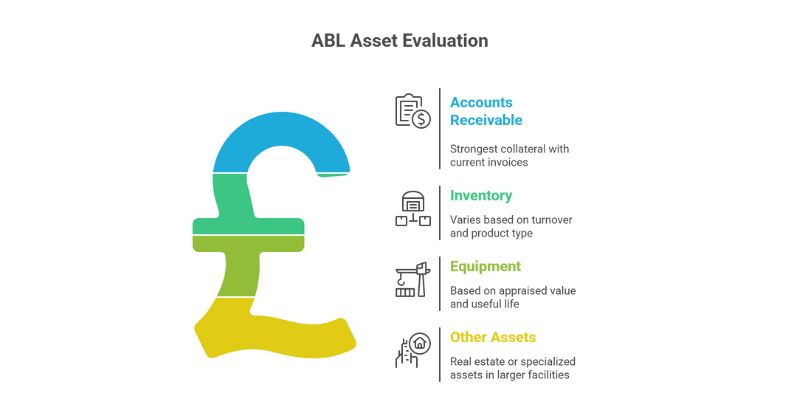

Eligible assets and advance rates

Not all assets are treated equally under an ABL structure. Lenders evaluate both quality and liquidity when determining advance rates. Common asset categories include:

- Accounts receivable: Typically the strongest collateral, especially when invoices are current and issued to creditworthy customers.

- Inventory: Advance rates vary depending on turnover, product type, and resale value.

- Equipment: Often included based on appraised value and remaining useful life.

- Other assets: Real estate or specialized assets may be included in larger facilities.

Advance rates generally range from high percentages on receivables to lower percentages on inventory and equipment. The exact structure depends on industry risk, customer concentration, and historical collection performance.

ABL versus receivables-focused financing

Businesses often compare ABL to receivables-only financing options when evaluating funding strategies. While both approaches unlock cash tied up in invoices, their structures differ significantly.

Working with an accounts receivable financing company usually involves securing a line of credit specifically against outstanding invoices. The business retains ownership of the receivables and continues handling collections, while the lender maintains a security interest. This approach preserves customer relationships and offers predictable access to working capital.

By contrast, an accounts receivable factoring company typically purchases invoices outright and may assume responsibility for collections. Factoring can be faster to set up and may require less reporting, but it is often more expensive and more visible to customers. It is commonly used by smaller or newer businesses that lack the operational infrastructure for more complex facilities.

ABL sits at the higher end of this spectrum, combining receivables financing with additional asset classes and greater scalability.

Risk management and reporting

ABL is not a passive financing arrangement. Because lenders rely on asset values, they require regular visibility into the business’s financial health. This typically includes periodic reporting of receivables aging, inventory levels, and cash receipts.

While some business owners view reporting requirements as burdensome, strong internal controls often lead to better terms and higher advance rates. Transparent reporting also benefits management by improving cash forecasting and operational discipline.

From a risk perspective, ABL lenders monitor customer concentration, payment trends, and asset turnover. If asset quality declines, borrowing availability may be adjusted. For growing businesses, this reinforces the importance of diversified customers and consistent billing practices.

Pricing and cost considerations

The cost of an ABL facility generally includes interest on drawn amounts and various administrative fees. Interest rates are often competitive with traditional bank credit for companies with strong asset quality, though additional costs may apply for audits, collateral monitoring, and reporting.

While ABL may appear more complex than a standard loan, it often proves cost-effective when measured against the opportunity cost of constrained growth. The ability to accept larger orders, negotiate better supplier terms, or avoid equity dilution frequently outweighs the incremental administrative expense.

Industries best suited for ABL

ABL is particularly effective for businesses with tangible, recurring assets. Common industries include manufacturing, distribution, logistics, staffing, wholesale trade, and certain professional services with B2B invoicing models.

Companies with strong sales but limited hard assets may find other financing options more appropriate. However, for asset-rich businesses, ABL provides a financing framework that mirrors operational realities rather than forcing growth into rigid loan structures.

Preparing for an ABL facility

Businesses considering ABL can improve outcomes by preparing in advance. Clean financial statements, consistent invoicing procedures, and accurate inventory tracking all contribute to stronger borrowing bases. Reducing customer concentration and resolving disputed invoices can significantly increase eligible collateral.

Engaging with lenders early in the growth cycle also helps. Establishing an ABL facility before liquidity becomes critical allows for smoother onboarding and better terms.

The role of ABL in long-term strategy

ABL is not just a short-term cash flow solution. When structured correctly, it becomes a strategic growth tool. Many mid-market companies rely on ABL for years as they scale operations, enter new markets, or prepare for acquisitions.

As businesses mature, ABL facilities can evolve, incorporating additional assets or transitioning into hybrid structures that combine asset-backed revolvers with term debt. This adaptability makes ABL a foundational component of many long-term capital strategies.

Final thoughts

Scalable financing is essential for sustainable business growth, and Asset-Based Lending offers one of the most flexible and practical solutions available. By aligning funding availability with real assets, ABL removes many of the limitations imposed by traditional lending models.

For growing businesses facing increasing working capital demands, ABL provides predictability, speed, and scalability without sacrificing ownership or operational control. When paired with disciplined financial management and the right lending partner, it can be a powerful driver of long-term success.