If you have ever been turned down for funding because of your credit score, you already know how frustrating the process can be. You might have a business that is bringing in revenue, customers that pay on time, and plans to grow, yet the conversation ends the moment your credit gets pulled.

That is the traditional system. But it is not the only one anymore.

Lending has evolved. A lot of decisions today are not based purely on credit history. They are based on how your business actually performs right now. If you understand what lenders really look for, you can still get approved, even with a lower score.

This is where most business owners get it wrong. They assume bad credit means no funding. In reality, it just means you need a different approach.

Credit Scores Matter, But They Are Not the Whole Story

Let’s be honest. Credit still plays a role. It tells lenders how you have handled debt in the past. Missed payments, high balances, defaults, all of that shows up.

But here is what many people do not realize. A credit score is backward looking. Lending decisions are forward looking.

A lender is not just asking, “What happened before?”

They are asking, “Can this business repay going forward?”

That shift in thinking is why many businesses with credit scores under 600 still get funded today.

Banks tend to stay rigid. They rely heavily on credit thresholds. Alternative lenders and private funding companies look at the full picture. That includes revenue, assets, and operational stability.

So yes, low credit can slow things down. It does not shut the door.

What Lenders Actually Pay Attention To

When a file lands on an underwriter’s desk, credit is just one tab. The real decision comes from everything else.

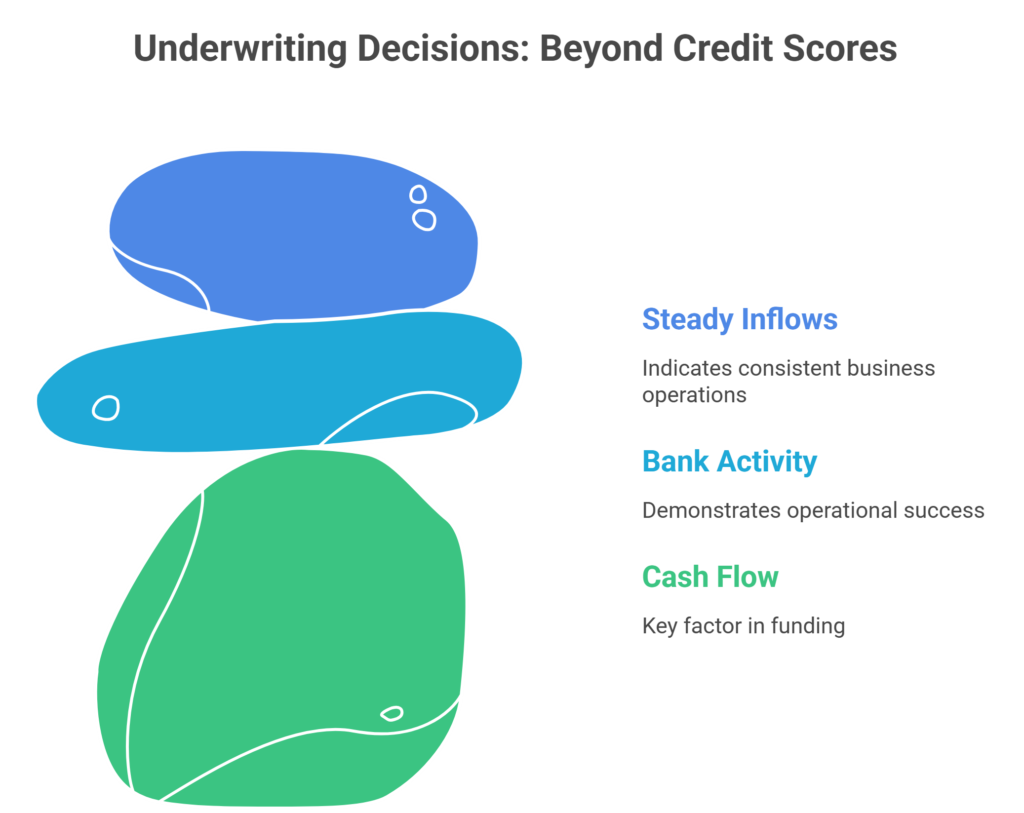

Cash Flow Comes First

If there is one thing that outweighs credit, it is cash flow.

A business that consistently brings in money is easier to fund than one that looks good on paper but struggles with deposits. Lenders want to see activity. Not just revenue on a tax return, but real movement in your bank account.

Steady inflows tell a simple story. This business operates. It sells. It collects.

That matters more than a perfect credit score.

Time in Business Still Carries Weight

A business that has been around for a while sends a strong signal. It shows resilience.

Startups can get funded, but they are riskier. A company that has been operating for three, five, or ten years has already proven it can survive different cycles.

Even with lower credit, longevity helps balance the risk.

Debt Is Looked at Closely

Too much existing debt is one of the fastest ways to get declined.

It is not just about how much you owe. It is about whether your current cash flow can realistically support another obligation.

If your margins are tight, lenders will notice. If your numbers show breathing room, that works in your favor.

Assets Change the Conversation

When there are assets involved, everything shifts.

Inventory, equipment, receivables, these give lenders something to work with. They reduce uncertainty.

This is why businesses with strong balance sheets often get approved even when credit is not ideal.

Practical Ways to Qualify Even with Low Credit

This is where strategy matters. You cannot approach funding the same way someone with a 750 score would. But you can absolutely position yourself to get approved.

Focus on Telling a Real Business Story

Lenders see thousands of applications. The ones that stand out are not the cleanest, they are the clearest.

Your numbers should make sense without explanation. Revenue, expenses, and cash flow should align.

If you are asking for funding, be specific about why. Expansion, payroll, inventory, bridging a gap. A clear purpose builds confidence.

Vague applications get ignored. Clear ones get attention.

Use an Account Factoring Company When Cash Is Stuck in Invoices

If your issue is not lack of revenue but slow-paying customers, this is one of the smartest routes.

Working with an Account Factoring Company allows you to turn unpaid invoices into immediate cash. Instead of waiting 30, 60, or 90 days, you get most of that money upfront.

What makes this powerful is that approval is not based on your credit. It is based on your customers.

If your clients are reliable payers, you can unlock funding without worrying about your own score.

For many service-based and B2B businesses, this solves cash flow problems almost instantly.

Consider an ABL Loan for Business

An ABL Loan for Business works differently from a traditional loan.

Instead of relying heavily on credit, the lender looks at what your business owns. That could be receivables, inventory, or equipment.

The loan is structured around those assets. The stronger they are, the more flexibility you get.

This type of financing is common in industries like manufacturing, distribution, and wholesale, where assets play a big role in operations.

It is not always the first option business owners think about, but it is often one of the most effective.

Pick the Right Lender from the Start

A lot of rejections happen simply because the borrower applied to the wrong place.

Here is a simple breakdown that reflects how things work in the real world:

| Lender Type |

How They View Credit |

What They Care About Most | Typical Outcome for Low Credit |

| Large Banks | Very strict | Credit history, financial ratios | Likely decline |

| Community Banks | Moderately strict | Relationship, local presence | Possible with strong profile |

| Online Lenders | Flexible | Cash flow, bank activity | Higher approval chances |

| Asset-Based Lenders | Least focused | Collateral and assets | Strong approval potential |

Choosing the right category from the beginning saves time and protects your credit from unnecessary pulls.

Clean Up What You Can Before Applying

You do not need perfect credit, but you should not ignore it either.

A few small steps can make a noticeable difference:

- Pay down high balances where possible

- Bring any past-due accounts current

- Check for reporting errors

- Avoid applying for multiple loans at once

Even modest improvements show lenders that you are making an effort to stabilize your finances.

Start Smaller Than You Think You Need

This is something experienced borrowers understand well.

If your credit is holding you back, asking for a large amount right away can hurt your chances. A smaller, manageable loan is easier to approve.

Once you repay it successfully, your profile improves. The next round of funding becomes easier and often comes with better terms.

It is a step-by-step process, not a one-time win.

Alternative Financing Options That Actually Work

When traditional loans are not a fit, these options fill the gap.

Small Business Loans in USA Through Nontraditional Lenders

There is a growing segment of lenders offering Small Business Loans in USA that focus less on credit scores and more on performance.

They review your bank statements, monthly deposits, and overall activity. If your business is generating consistent income, that carries weight.

The trade-off is cost. Rates are usually higher. But access to capital can help you stabilize and grow, which matters more in the long run.

Lines of Credit for Flexibility

A line of credit gives you access to funds without forcing you to use everything at once.

You draw what you need, repay it, and use it again. This is especially helpful if your cash flow fluctuates during the year.

Merchant Cash Advances for Short-Term Needs

This option is fast and relatively easy to qualify for.

Repayment is tied to your daily or weekly sales. That makes it flexible, but also more expensive.

It is best used carefully, usually for short-term gaps rather than long-term financing.

Microloans and Local Programs

Some funding sources take a more personal approach. They look at your experience, your business model, and your goals.

If your business serves a community need or shows strong growth potential, these programs can be a good fit.

Regional Programs Can Open Unexpected Doors

Many business owners overlook local funding opportunities.

For example, California Small Business Loans programs often include state-backed initiatives that are designed to support businesses that may not qualify through traditional channels.

These programs sometimes offer better terms, lower rates, or more flexible approval criteria.

It takes a bit of research, but it can be worth the effort.

Mistakes That Quietly Hurt Your Chances

Not all rejections come from bad credit. Some come from avoidable issues.

Applying without preparation is one of them. If your documents are incomplete or inconsistent, lenders lose confidence quickly.

Another common issue is overstating revenue. Lenders verify everything. If numbers do not match, it raises concerns immediately.

Ignoring cash flow problems is another big one. Strong sales mean very little if expenses are eating up most of the income.

Clean, honest, and well-prepared applications always perform better.

The Trade-Off Is Real, But Manageable

There is no way around this part. Lower credit usually means higher costs.

You may see:

- Higher interest rates

- Shorter repayment periods

- Additional fees

But this does not automatically make the funding a bad decision.

If the capital helps you take on more business, increase revenue, or stabilize operations, it can still be a smart move.

The key is using the funds with a clear plan, not just to cover gaps, but to improve your position.

Final Thoughts

Low credit does not disqualify you from business lending. It just changes the path you take.

The businesses that succeed in getting funded are not the ones with perfect scores. They are the ones that understand how to present their strengths.

Focus on what you can control. Your cash flow, your documentation, your strategy, and the type of lender you approach.

There is always a way forward. You just have to approach it differently.