B2B commerce has always relied on trade credit. A supplier delivers goods or services today, but payment typically arrives 30, 60, or even 90 days later. For many companies, especially growing ones, that waiting period creates a major operational challenge. Payroll, rent, inventory purchases, and transportation costs must be paid immediately, while revenue remains locked inside unpaid invoices.

In recent years, invoice factoring startups have emerged as a powerful response to this long-standing problem. What was once a specialized funding method handled by a small segment of finance firms has transformed into a technology-driven financing ecosystem. Instead of waiting months for payments, businesses can convert invoices into working capital almost instantly.

The scale of this change is significant. The global factoring industry now handles transactions worth several trillions of dollars annually, and it continues to grow each year as more companies rely on credit-based transactions. The growth is not simply due to economic expansion; it reflects a change in how businesses manage liquidity. Rather than depending on loans, companies increasingly finance cash flow directly through their sales activity.

Why Cash Flow Became a Critical Business Issue

Profitability and cash flow are not the same thing. A business can be profitable on paper yet struggle to operate because its customers pay late. In B2B industries, delayed payments are extremely common. Many companies extend credit to remain competitive, especially when dealing with large buyers who negotiate longer payment terms.

This creates a predictable cycle:

- Sales increase

- Receivables increase

- Operating costs increase

- Cash availability decreases

Rapid growth often makes the situation worse. A business winning more contracts must hire employees, purchase materials, and cover operational expenses before receiving payment. Traditional financing options, particularly bank loans, do not always solve the problem because approval depends on financial history, collateral, and strict underwriting standards.

Invoice factoring startups address a different question than banks. Instead of asking whether the seller qualifies for credit, they evaluate whether the customer paying the invoice is reliable. That single shift opened financing to a wider group of companies.

How Modern Factoring Startups Operate

Factoring is based on a straightforward concept. A company sells its unpaid invoices to a funding provider and receives most of the invoice value immediately. Once the customer pays the invoice, the remaining balance is released to the business after fees.

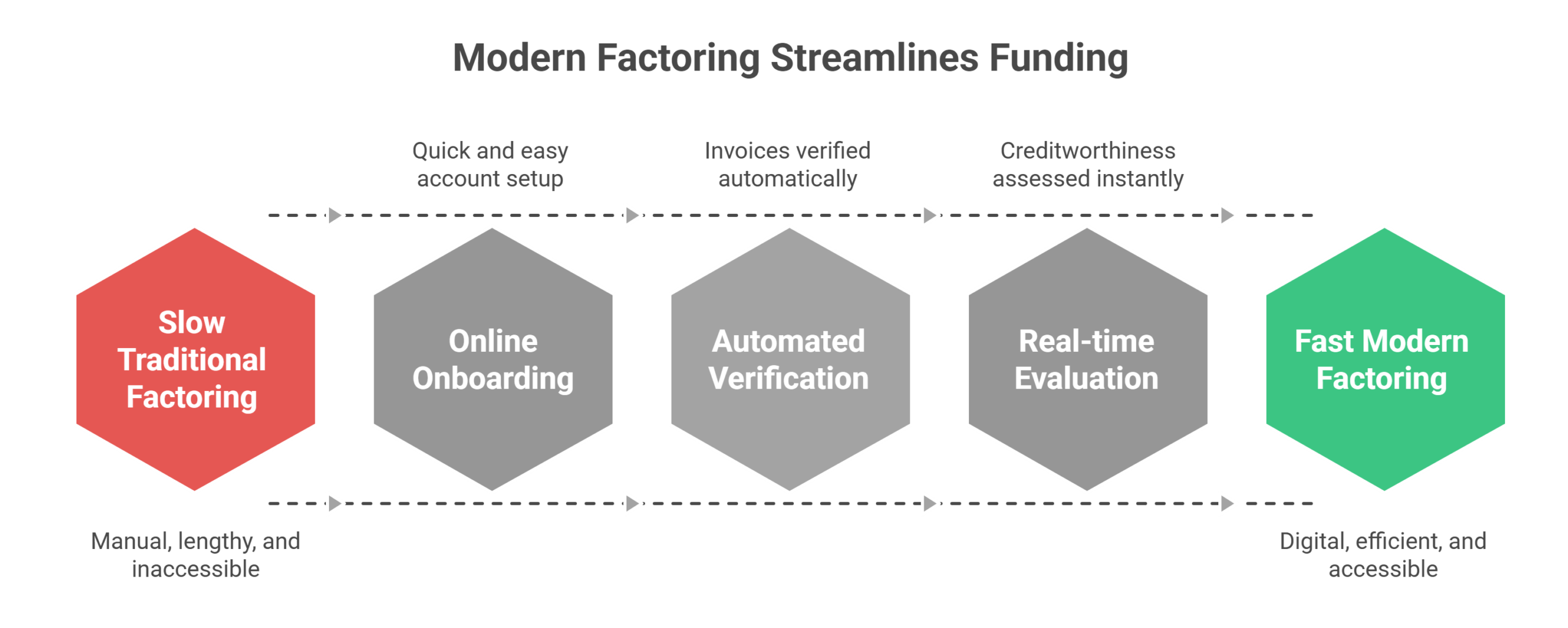

What startups changed was the speed and accessibility of the process.

Traditional factoring required:

- physical documentation

- manual verification

- long approval timelines

- detailed financial reviews

Modern platforms use digital tools:

- accounting software integrations

- automated invoice verification

- online onboarding

- real-time credit evaluation

Today, a business can upload invoices, receive approval, and obtain funding within a day. In many cases, platforms connect directly with accounting systems, allowing invoices to be verified automatically. This reduces paperwork and allows providers to serve smaller businesses efficiently.

Technology Is the Driving Force

The rise of fintech is the main reason factoring has expanded so quickly. Technology enables providers to analyze transaction data instead of relying only on financial statements. Payment behavior, customer creditworthiness, invoice history, and sales patterns can all be evaluated quickly using automated systems.

Digital underwriting lowers operating costs for providers. Because administrative expenses decrease, smaller transactions become economically viable. That means companies no longer need large funding requirements to qualify.

Automation also improves risk management. Platforms track payment patterns and identify late-pay trends. Some systems even predict delays before they occur. The result is a financing model based on real economic activity rather than projections.

Why Businesses Prefer This Model

One of the main advantages of factoring startups is flexibility. Traditional loans create fixed repayment schedules. Factoring works differently funding grows with sales volume.

When a company invoices more customers, available funding automatically increases. When sales slow, financing usage decreases. Businesses do not carry unused debt or pay interest on capital they are not using.

Companies choose this structure because it supports operations directly. Instead of borrowing based on past performance, they access funds based on current activity.

Key benefits include:

- improved cash flow stability

- ability to accept larger orders

- timely payroll payments

- stronger supplier relationships

- reduced dependence on credit lines

For many growing companies, the biggest risk is not lack of demand but inability to support expansion. Immediate liquidity removes that obstacle.

The Shift Away From Traditional Lending

Banks remain important financial partners, but they are not always structured to support rapidly scaling businesses. Strict regulations, collateral requirements, and lengthy underwriting processes limit their ability to provide short-term operational funding.

Invoice factoring startups stepped into this gap. Their operating model focuses on transactions rather than balance sheets. Because invoices represent completed work or delivered goods, they provide a measurable asset.

An accounts receivable financing company evaluates the credit quality of the customer responsible for payment. If the buyer is reliable, the invoice becomes financeable regardless of how young the supplier business may be.

This model especially benefits:

- startups

- staffing agencies

- logistics providers

- distributors

- manufacturers

These industries commonly operate with thin margins and long payment cycles, making predictable cash flow essential.

Specialization and Industry Focus

As competition increased, providers began specializing in certain sectors. Instead of serving every type of company, many firms now tailor programs to industries with consistent invoicing structures.

Receivables factoring companies often focus on specific verticals such as transportation, construction subcontracting, medical billing, or wholesale trade. Specialization allows providers to understand payment behavior, contract structures, and operational risks within each industry.

For example, staffing companies rely heavily on weekly payroll cycles. Logistics companies must pay drivers and fuel costs immediately. Manufacturing suppliers must purchase raw materials before receiving payment. Each industry benefits from funding aligned with operational timing.

This targeted approach has made factoring more efficient and accessible.

The Role of Embedded Finance

Another major development is embedded finance. Rather than applying for funding separately, businesses now encounter financing within the platforms they already use.

Accounting software, payment processors, and supply-chain platforms increasingly offer funding directly after an invoice is created. The system detects an eligible invoice and presents a funding option automatically.

This integration reduces friction. Businesses do not need to search for lenders, complete lengthy applications, or provide repeated documentation. Financing becomes part of the workflow instead of a separate process.

Embedded finance also explains why adoption has accelerated. Companies are not actively seeking financing they are accepting a convenient operational tool.

Impact on Small and Mid-Sized Businesses

Small and mid-sized businesses are the primary beneficiaries of the factoring startup movement. These companies typically lack large cash reserves and face payment delays from larger customers. Yet they also represent a major portion of economic activity and employment.

Factoring allows them to:

- stabilize working capital

- manage growth

- reduce financial stress

- avoid excessive borrowing

Many companies previously relied on personal savings, credit cards, or delayed vendor payments. With factoring, operational expenses are covered by revenue that has already been earned but not yet received.

As awareness increases, business owners now compare multiple providers and evaluate service quality, technology integration, and industry expertise when selecting the best invoice factoring companies.

Global Trade and Cross-Border Commerce

International trade has also accelerated adoption. Exporters frequently wait longer for payment due to shipping times, customs procedures, and currency settlement. Factoring provides immediate local currency while the financier manages collection.

This is particularly valuable for suppliers working with overseas buyers or large retail chains. Immediate payment improves purchasing power and allows businesses to negotiate better supplier terms.

E-commerce supply chains, wholesale imports, and manufacturing exports increasingly rely on receivable-based funding because traditional international lending is slower and documentation-heavy.

Risk Management and Data-Driven Decisions

Startups have improved risk management through data analytics. Instead of relying solely on credit reports, providers evaluate real transaction behavior. They analyze:

- payment frequency

- customer reliability

- invoice size patterns

- seasonal variations

Because funding is tied to completed transactions, risk is measurable and controllable. Providers can adjust advance rates or eligibility dynamically as payment trends change.

This approach protects both the financier and the business. Companies gain funding without overextending themselves, while providers maintain portfolio stability.

The Future of B2B Financing

The continued expansion of factoring startups suggests a long-term transformation in business finance. Rather than borrowing money and repaying it later, companies increasingly monetize revenue as it is generated.

Future developments may include:

- automatic payments immediately after invoicing

- predictive cash-flow forecasting tools

- dynamic credit limits based on sales activity

- integrated accounting and funding platforms

In this model, financing becomes an operational service rather than a separate financial decision.

Final Perspective

Invoice factoring startups have changed the foundation of working-capital financing. By focusing on real transactions instead of historical financial strength, they expanded access to liquidity for growing companies.

Businesses no longer need to pause operations while waiting for payments. Revenue can support operations immediately, allowing companies to scale faster, meet obligations confidently, and pursue larger opportunities.

As trade credit remains a central feature of B2B commerce, receivable-based financing will continue evolving. What began as an alternative funding option is now becoming a standard financial tool one that aligns financing directly with economic activity and modern business operations.