Running a business means constantly making critical decisions about growth, operations, and finances. One of the most important choices a business owner must make is selecting the right type of funding. Among the many options, term loans are a common and reliable choice. But how can you determine if a term loan is the best fit for your business?

In this guide, we’ll break down what term loans are, how they function, their advantages and potential drawbacks, and offer guidance on deciding if this financing option aligns with your business goals.

What Is a Business Term Loan?

A business term loan is a lump sum of money borrowed from a lender that is repaid over a fixed period, typically with monthly payments that include principal and interest. Term loans differ from lines of credit, which allow you to borrow, repay, and re-borrow funds. With a term loan, once you borrow the funds, you repay them on a set schedule until the balance is fully paid.

Term loans are versatile and available through traditional banks, credit unions, online lenders, and alternative financing providers. They can range from short-term loans lasting less than two years to long-term loans extending five years or more. The structure of a term loan including interest rates, repayment schedules, and fees depends on the lender and the borrower’s creditworthiness.

Who Should Consider a Term Loan?

Term loans can be beneficial for a wide range of businesses, but they are particularly useful when you have a specific, one-time funding need. Common scenarios include:

- Expansion projects: Opening a new location, launching a product line, or entering new markets.

- Equipment purchases: Investing in machinery, vehicles, computers, or other operational tools.

- Working capital needs: Covering day-to-day expenses, particularly during seasonal slowdowns or cash flow gaps.

- Debt consolidation: Refinancing higher-cost debt to improve cash flow management.

For businesses that need structured financing with predictable repayment schedules, a term loan is often a strong option. Businesses that rely on fluctuating revenue streams may need to carefully consider whether a fixed repayment schedule fits their cash flow situation.

Understanding the Basics of Term Loans

Before applying for a term loan, it’s essential to understand the key components:

Loan Amount and Term Length

Term loans can range from as little as $5,000 to millions of dollars, depending on your business size and lender requirements. Short-term loans typically span less than two years, while long-term loans can extend five years or more. The loan amount and term length should align with your business goals and repayment capacity.

Interest Rates

Interest rates vary based on lender type, loan term, and the borrower’s credit profile. Traditional banks often offer lower rates but have more stringent qualification requirements. Online and alternative lenders can provide faster access to funds but may charge slightly higher rates.

Repayment Schedule

Most term loans follow a structured repayment plan, with equal monthly installments covering both principal and interest. While some lenders allow early repayment, certain loans may include prepayment penalties.

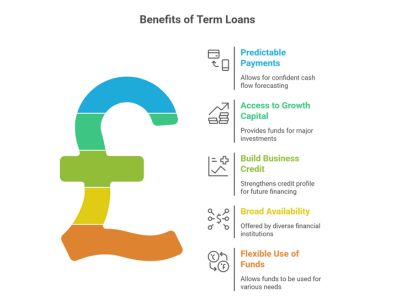

Advantages of Term Loans

Term loans offer several benefits that make them appealing to business owners:

1. Predictable Payments

With fixed monthly payments, businesses can forecast cash flow and plan budgets with confidence. This stability is particularly helpful for companies looking to invest in long-term growth initiatives.

2. Access to Growth Capital

Term loans can provide significant capital needed for major investments, whether it’s buying equipment, expanding facilities, or entering new markets.

3. Build Business Credit

Timely repayment of a term loan can strengthen your business credit profile, improving access to financing in the future.

4. Broad Availability

Term loans are offered by a variety of financial institutions, including traditional banks, online lenders, and alternative finance providers. This diversity increases the likelihood of finding a loan that meets your needs.

5. Flexible Use of Funds

Unlike some forms of financing tied to specific purposes, term loans typically offer flexibility in how the funds are used, allowing businesses to address their most pressing needs.

Potential Drawbacks of Term Loans

While term loans have many benefits, they may not be suitable for every business. It’s important to consider potential challenges:

1. Fixed Repayment Obligation

Term loans require consistent payments regardless of revenue fluctuations. Businesses with seasonal or unpredictable income may find these payments challenging.

2. Collateral Requirements

Many lenders require collateral to secure a term loan. This could be property, equipment, or other business assets, which can be at risk if repayments are missed.

3. Longer Approval Process

Traditional banks and credit unions may require extensive documentation and underwriting, resulting in a longer approval timeline compared with alternative financing options.

4. Total Interest Cost

While monthly payments are predictable, the total interest paid over the life of the loan can be substantial, especially for long-term loans. Businesses should calculate the overall cost of borrowing before committing.

Exploring the Broader Financing Landscape

Term loans are one piece of the larger business financing ecosystem. Many companies explore a combination of funding options to meet their specific needs.

For example, businesses with unpaid invoices might consider partnering with an accounts receivable financing company. This option allows companies to access cash tied up in unpaid invoices, improving short-term cash flow without taking on long-term debt.

Additionally, small businesses across the United States often weigh various sources of funding, including grants, lines of credit, equipment financing, and SBA-backed loans. Understanding the differences in these options is critical to choosing the right path.

How to Decide if a Term Loan Is Right for Your Business

Here are practical steps to determine whether a term loan fits your business:

1. Identify the Purpose

Clarify why you need the funds. Term loans work best for well-defined needs such as expansion, equipment purchases, or debt consolidation, rather than ongoing operational expenses.

2. Assess Financial Health

Evaluate your cash flow, revenue stability, and existing debt obligations. Lenders often consider these factors when approving a loan and setting interest rates.

3. Match Loan Term to Need

Short-term loans are suitable for temporary needs or quick growth opportunities, while long-term loans support larger, strategic investments. Aligning the loan term with the purpose ensures manageable repayment.

4. Compare Financing Options

Don’t limit yourself to term loans. Consider alternative options such as lines of credit, equipment financing, or invoice factoring. Each type of financing has distinct advantages depending on your cash flow and operational priorities.

5. Analyze Costs and Terms

Look beyond monthly payments. Consider the interest rate, fees, prepayment penalties, and collateral requirements. Understanding the total cost of borrowing is essential for making an informed decision.

Regional Considerations: Loans in California and the U.S.

Business financing dynamics can vary depending on your location. For example, businesses seeking small business loans California may find competitive lending rates due to the state’s robust economy and high concentration of small businesses. However, lenders in California can also have stricter requirements compared with other regions.

On a broader scale, small business loans USA reflect a diverse landscape. Approval rates, interest rates, and lending standards vary by state, lender type, and industry. National trends indicate that small businesses increasingly access funding through online platforms and alternative financing providers alongside traditional banks, providing more options to match specific needs.

Real-World Example: Using a Term Loan

Consider a small manufacturing company that wants to purchase new machinery to increase production efficiency. The equipment costs $200,000, and the business projects a 15% increase in output within a year.

The company secures a five-year term loan:

- Loan amount: $200,000

- Term: 5 years

- Interest rate: Fixed at a competitive rate with monthly payments

The term loan enables the company to purchase the equipment immediately, increase productivity, and repay the loan through increased revenue, all while maintaining operational cash flow.

Key Takeaways

Term loans remain a foundational financing option for businesses of all sizes. They provide structured funding, predictable repayments, and access to capital for long-term investments. However, they also require careful planning, as fixed repayment schedules and potential collateral requirements can be challenging for businesses with variable cash flow.

Before committing, ask yourself:

- Do I have a clear, specific purpose for the loan?

- Can my business handle the repayment schedule?

- Are the terms and costs aligned with my growth goals?

If your business is financially stable and you have a defined need for capital, a term loan could be the right solution to fuel expansion, purchase critical equipment, or consolidate debt.

Final Thoughts

Choosing the right funding path is critical for your business’s growth and stability. Term loans offer the predictability, structure, and capital access many businesses need to reach their next stage. By carefully analyzing your financial health, repayment capacity, and funding goals, you can determine whether a term loan is the optimal choice or if alternative financing options may better suit your business strategy.

The key is to make a well-informed decision, align your financing with your business objectives, and leverage available resources to support sustainable growth.