Healthcare organizations operate in one of the most complex financial environments today. Hospitals, private practices, surgery centers, diagnostic labs, dental groups, home care agencies, and behavioral health facilities all share a common challenge: cash flow volatility. Insurance claim processing delays, billing complexities, denied reimbursements, seasonal patient fluctuations, and high upfront operating expenses can make it difficult for providers to maintain steady liquidity. For many, a healthcare asset-based loan becomes a vital financial lifeline.

This detailed guide explains what healthcare asset-based loans are, how they work, and most importantly what healthcare providers need to do to qualify for them. By the end, you’ll understand the eligibility standards, documentation requirements, underwriting considerations, and practical strategies for boosting approval odds.

The Role of Asset-Based Lending in Healthcare

Healthcare asset-based loans are structured forms of Asset based Lending that are collateral-driven rather than credit-driven. Instead of relying solely on credit scores or long-term profitability, lenders evaluate the value and quality of assets such as accounts receivable, medical equipment, inventory, or real estate.

Because healthcare providers frequently wait 45–90 days for reimbursement longer if claim disputes arise accounts receivable become extremely valuable collateral. These unpaid claims represent guaranteed future revenue once insurers process them. Asset-based financing allows providers to borrow against this receivable pool to cover immediate operational needs.

For many healthcare organizations, this type of financing is more accessible than traditional bank loans, which often require strong net income, high credit scores, significant cash reserves, and clean financial statements criteria that many expanding or cash-constrained providers cannot meet consistently.

Why Providers Seek Healthcare Asset-Based Loans

Healthcare providers commonly pursue asset-based loans for reasons such as:

- Working capital to cover payroll, rent, and utilities

- Covering operational gaps caused by delayed reimbursements

- Upgrading or acquiring medical equipment

- Expanding clinics or opening new service lines

- Funding acquisitions or mergers

- Purchasing medical supplies or pharmaceuticals

- Managing seasonal or volume-based patient fluctuations

In addition, providers in growth mode may onboard physicians, expand specialties, increase patient throughput, or add new insurance contracts all activities that increase receivables but strain cash flow in the short term.

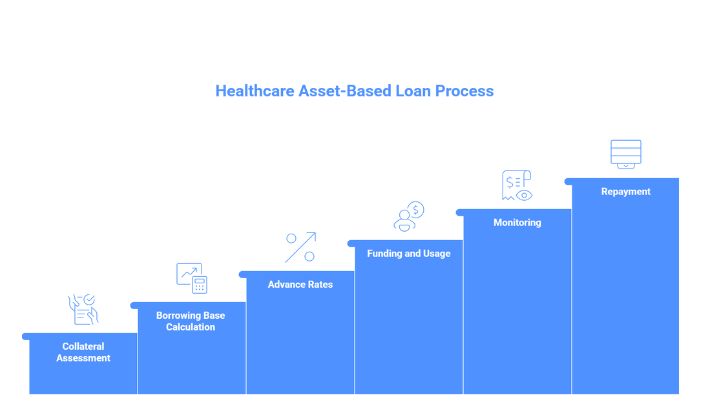

How Healthcare Asset-Based Loans Work

While terms may vary by lender, most healthcare asset-based loans follow a similar structure:

- Collateral Assessment: The lender evaluates eligible collateral, usually starting with accounts receivable.

- Borrowing Base Calculation: The lender applies eligibility criteria (aging limits, payer mix, denial rates, and claim quality) to determine how much of the receivable pool can be financed.

- Advance Rates: The lender advances a percentage often 70–90% against eligible receivables.

- Funding and Usage: The provider draws funds as needed for operational expenses.

- Monitoring: The lender periodically reviews receivables performance to update eligible advance amounts.

- Repayment: Funds are repaid as receivables convert into cash through insurance reimbursements.

Unlike loans with fixed installment payments, healthcare asset-based lending facilities often behave like revolving credit lines linked to the provider’s receivable volume. As receivables grow, the borrowing base grows; as receivables decline, the available credit decreases.

Key Assets Used as Collateral

Most healthcare asset-based credit lines are backed by:

1. Accounts Receivable

Receivables from Medicare, Medicaid, commercial insurance carriers, HMOs, PPOs, workers compensation, and sometimes patients.

2. Equipment

Diagnostic machines, medical imaging equipment, lab analyzers, treatment devices, and surgical tools can be appraised for collateral value.

3. Inventory

Pharmaceuticals, medical supplies, protective equipment, and specialty inventory may be included in certain structures.

4. Real Estate

Owned clinics, surgery centers, or administrative buildings can improve collateral strength and increase funding capacity.

Not every lender accepts all asset classes; most weigh receivables most heavily due to their predictable and monetizable nature.

Core Qualification Requirements

Now let’s break down what lenders typically require to approve a healthcare asset-based loan.

1. Strong Accounts Receivable Quality

The single most important qualification factor is the strength of the provider’s accounts receivable portfolio. Lenders assess:

- Aging: Claims under 90–120 days are more desirable; older claims reduce eligibility.

- Payer Mix: Insurer-backed receivables are viewed as more secure than patient-pay receivables.

- Denial Rates: High denial or appeal rates suggest cash flow risk.

- Billing Efficiency: Clean, fast claims processing increases collectibility.

- Concentration: Heavy reliance on a single insurer creates concentration risk.

Providers with diversified insurers, low denial rates, and efficient billing systems are viewed favorably.

2. Reliable Billing and Collections Systems

Providers should demonstrate:

- Accurate coding practices

- Timely claim submissions

- EMR/EHR integration with billing systems

- Low administrative backlogs

- Transparent revenue cycle workflows

Lenders may request process documentation or audit billing performance to confirm receivable integrity.

- Sufficient Financial Reporting Infrastructure

While asset-based lenders are more flexible than traditional banks, they still require structured financial reporting. Typical documentation includes:

- Accounts receivable aging reports

- Monthly financial statements (P&L, balance sheet, cash flow)

- Insurance reimbursement histories

- Payer concentration reports

- Equipment inventories and valuations

- Corporate tax returns

- Organization charts and ownership details

Providers lacking organized reporting may struggle to qualify due to underwriting uncertainty.

4. Compliance and Regulatory Standing

Healthcare is highly regulated, so lenders require confirmation of compliance with state, federal, and accreditation standards. Providers must have:

- Valid licenses and certifications

- No outstanding Medicare or Medicaid sanctions

- No significant fraud investigations

- Clean regulatory history

- Accurate credentialing and provider enrollment documentation

Compliance risk directly influences underwriting outcomes.

5. Operational Stability and Management Strength

Lenders evaluate the quality of leadership and governance. This includes:

- Executive and financial management experience

- Track record of operational performance

- Strategic planning capability

- Staff retention and staffing stability

- Practice longevity and historical performance

Strong leadership improves approval likelihood and may unlock better lending terms.

Factors That Strengthen Approval Odds

Providers can take several proactive steps to enhance their qualification profile.

Improve Revenue Cycle Management

Investing in claims scrubbing, denial management, and EMR billing integration can increase receivable quality and shorten reimbursement cycles.

Diversify Payer Mix

Heavy reliance on a single commercial carrier or government program creates risk. Diversification boosts receivable stability.

Reduce AR Aging

Cleaning up older receivables increases the eligible borrowing base and demonstrates operational control.

Enhance Financial Reporting

Timely, accurate financial statements instill lender confidence and support better loan structures.

Document Asset Values

Up-to-date equipment appraisals, real estate valuations, and inventory lists accelerate underwriting.

How Asset-Based Loans Compare to Other Funding Options

Healthcare organizations also consider alternatives such as factoring, merchant cash advances, traditional bank loans, credit cards, and private equity. Factoring is often offered by specialized receivables factoring companies, where invoices are sold to free up capital. In contrast, asset-based loans allow providers to retain ownership of receivables and borrow against them for flexible liquidity.

On the other hand, some organizations explore partnerships with receivables financing companies, which offer structured advances based on expected reimbursement flows without requiring invoice sales or recourse arrangements. These models tend to appeal to providers with moderate receivable volumes and predictable reimbursement timelines.

Conclusion: A Strategic Path to Healthcare Liquidity

Qualifying for a healthcare asset-based loan requires preparation, but it is achievable for many organizations when the right elements are in place. Providers with strong receivables, reliable billing systems, sound documentation, and regulatory compliance have a powerful advantage in securing approval.

Healthcare continues to evolve, reimbursement cycles remain lengthy, and operational costs are rising. Asset-based lending empowers providers to stabilize cash flow, support staff, maintain patient care quality, seize growth opportunities, and navigate an industry where financial predictability is rare.

For organizations looking to strengthen financial resilience while preserving ownership and operational control, healthcare asset-based loans represent one of the most strategic funding solutions available today.