For decades, business liquidity was largely defined by traditional bank lending. If a company had strong credit, steady profitability, and years of financial history, it could access working capital. If it didn’t, funding was either delayed or denied.

Today, that model is changing.

Businesses operate in an environment where operating costs, payroll, vendor obligations, and expansion investments must be supported by reliable cash flow. Many organizations generate strong sales yet still face pressure because the money tied to operations is not immediately accessible. As a result, companies are increasingly turning toward asset-backed funding a financial structure that converts existing business assets into usable working capital.

Asset-backed funding is not just an alternative to traditional loans. It is redefining what liquidity means in practical business terms.

The Real Liquidity Challenge Businesses Face

Profitability and liquidity are not the same thing.

A company can report healthy revenue while still struggling to cover everyday obligations such as supplier payments, employee wages, or operational expenses. The issue is not lack of sales; the issue is accessibility of funds.

This creates a cash flow imbalance:

- Expenses occur continuously

- Revenue recognition happens on paper

- Operational costs require immediate payment

When capital remains tied inside operational transactions, growth slows and planning becomes difficult. Businesses often delay hiring, purchasing, or expansion simply because funds are temporarily unavailable.

This is where asset-backed funding changes the equation.

What Asset-Backed Funding Really Means

Asset-backed funding allows businesses to access capital using the value of their existing assets rather than relying entirely on credit scores or long financial histories.

Common assets used as collateral include:

- Accounts receivable

- Inventory

- Equipment

- Purchase orders

- Contracted future revenue

Under Asset based Lending, financing is structured around the measurable value of these operational assets. Instead of focusing only on past financial statements, lenders analyze the quality and reliability of the collateral supporting the transaction.

For instance, if a company has completed work for a reputable customer, the resulting invoice holds real economic value. Rather than waiting for the payment cycle to conclude, the business can obtain funding against that asset and continue operating smoothly.

This approach transforms working capital management from reactive to strategic.

Market Growth and Industry Momentum

The growth of asset-backed funding reflects a broader change in business finance.

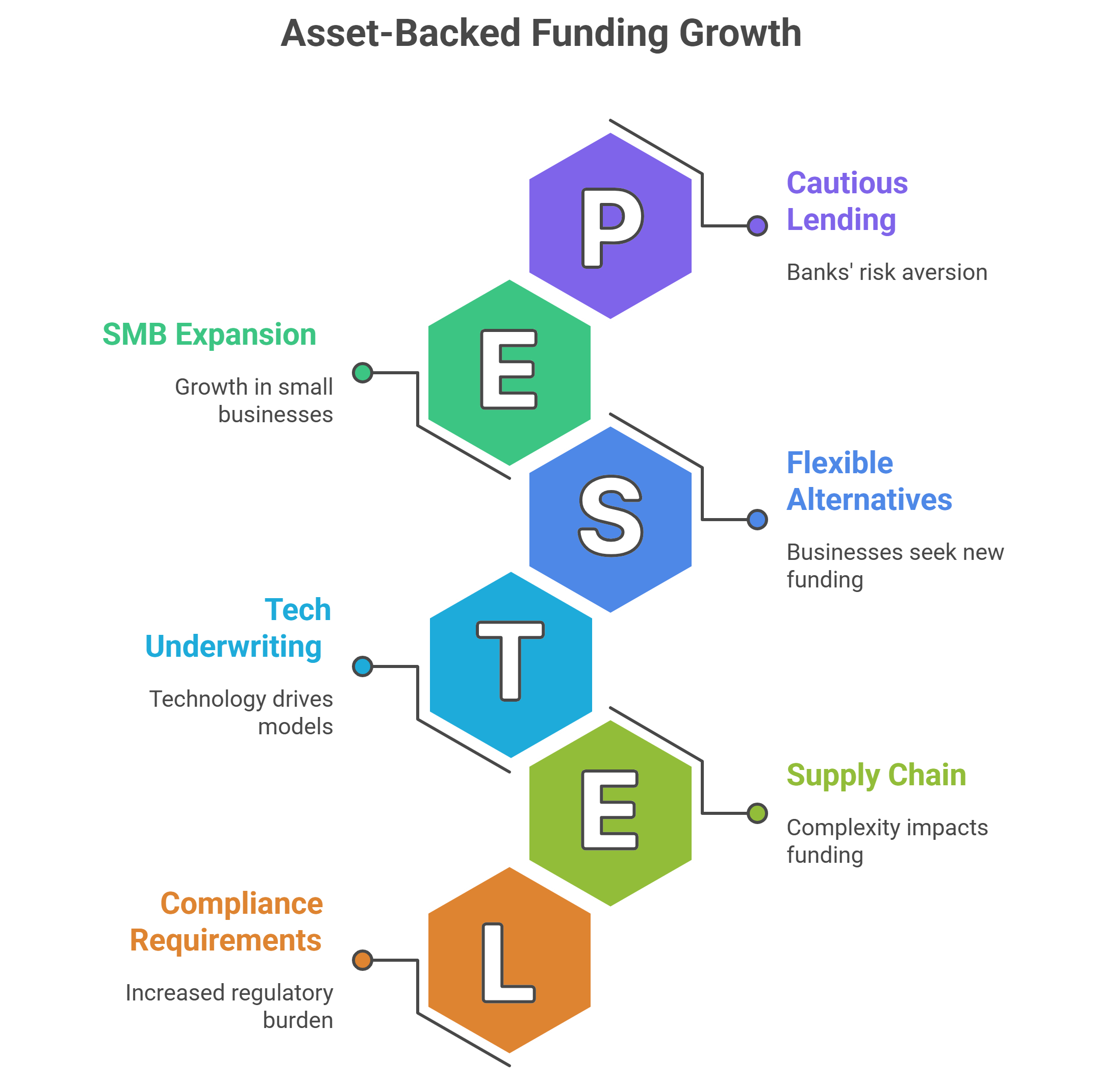

The global asset-based lending sector now exceeds a trillion dollars in annual activity and continues to expand at a steady rate. Analysts project continued double-digit growth as businesses seek flexible funding alternatives outside conventional lending channels.

Several factors are driving this expansion:

- More cautious lending practices by traditional banks

- Increased compliance requirements in commercial finance

- Rapid expansion of small and mid-sized companies

- Supply chain complexity

- Technology-driven underwriting models

Receivables-based financing has emerged as one of the most widely used forms of asset-backed funding because it is directly linked to revenue generation. Businesses consistently produce invoices, making them reliable financial assets.

Why Traditional Lending No Longer Fits Growth Companies

Traditional loans were designed for stable companies with long operating histories and conservative growth patterns. However, many modern businesses expand faster than traditional credit models are designed to support.

A distributor, staffing agency, or logistics provider may experience rapid revenue increases while maintaining thin profit margins. Conventional underwriting often interprets this as risk.

Asset-backed funding evaluates the situation differently. Instead of limiting capital due to historical ratios, funding capacity increases as operational activity increases. Growth strengthens borrowing capacity rather than restricting it.

This model is particularly effective for:

- Staffing firms

- Manufacturers

- Transportation companies

- Wholesale distributors

- Service providers with corporate clients

In these industries, large receivable balances are normal. Financing tied directly to those balances creates immediate liquidity.

Converting Receivables Into Usable Capital

One of the most transformative components of this financing approach is receivables financing.

An experienced accounts receivable financing company reviews outstanding invoices and advances a percentage of their value to the business. When the customer fulfills the payment obligation, the remaining balance is provided after agreed fees.

This provides several benefits:

- Faster access to working capital

- Reduced dependency on credit history

- Funding that grows alongside sales

- Improved financial predictability

Companies can meet payroll, pay suppliers, and accept new projects without waiting for funds to cycle back through operations.

The Strategic Role of Factoring

Factoring is another important structure within asset-backed funding. In this arrangement, invoices are sold to a financing provider in exchange for immediate capital.

A professional account factoring company often manages payment collection and receivable monitoring as part of the service. This removes administrative burden from business owners and improves cash management processes.

Factoring is particularly helpful for companies facing:

- Rapid expansion

- Seasonal revenue changes

- High payroll obligations

- Large contract opportunities

Because funding is tied to real transactions, businesses can stabilize operations and plan with greater confidence.

Technology Is Accelerating Liquidity Access

Technological advancement has dramatically improved the efficiency of asset-backed funding.

Modern platforms use:

- Automated verification of receivables

- Digital documentation

- Online reporting dashboards

- Data-driven risk evaluation

Funding approvals that once required extensive review can now occur quickly. This efficiency allows businesses to respond to opportunities without operational disruption.

Why Small and Mid-Sized Businesses Benefit Most

Small and mid-sized enterprises make up the majority of businesses worldwide, yet they often experience the most difficulty obtaining traditional credit. Limited financial history or retained earnings may restrict borrowing capacity even when operations are strong.

Asset-backed funding addresses this gap by focusing on operational strength instead of historical performance.

If a business has customers, contracts, and consistent activity, it can often access working capital. This enables companies to expand earlier in their life cycle and compete with larger organizations.

Liquidity as a Competitive Advantage

Forward-thinking companies no longer view financing as a last-resort measure. They use it strategically to strengthen operations.

Consistent liquidity enables businesses to:

- Secure bulk purchasing discounts

- Expand service offerings

- Increase production capacity

- Enter new markets

- Hire skilled staff promptly

Organizations with stable cash flow can make decisions based on opportunity rather than financial constraint.

Liquidity becomes a tool for growth rather than merely a safety net.

Risk Management and Financial Stability

Asset-backed funding also improves financial stability.

Traditional loans typically require fixed payments regardless of operational performance. When revenue fluctuates, repayment obligations remain constant.

Asset-backed structures are more adaptable. Funding capacity is tied to real business activity, which naturally adjusts over time. This reduces financial pressure and helps businesses avoid excessive debt commitments.

Additionally, because the financing is secured by tangible assets, lenders often remain supportive during transitional periods such as restructuring, mergers, or expansion.

The Future of Business Liquidity

The financial industry is gradually shifting toward cash-flow-based evaluation rather than strict credit-only models. Non-bank lenders, private credit providers, and specialized finance companies are expanding their participation in asset-backed markets.

This diversification increases capital availability and gives businesses more options when planning growth strategies.

As digital tools continue to enhance transparency and efficiency, asset-backed funding will likely become a standard component of corporate finance rather than an alternative solution.

Final Thoughts

Asset-backed funding is fundamentally redefining business liquidity.

In earlier financial models, liquidity depended heavily on accumulated reserves or traditional bank credit lines. Today, it depends on the ability to convert active business operations into working capital.

By leveraging invoices, inventory, and operational assets, companies can support expansion, stabilize cash flow, and operate more confidently.

Revenue no longer remains tied up within the operating cycle.

Assets no longer remain idle on financial statements.

Instead, businesses gain access to capital aligned with their real economic activity allowing them to grow, invest, and compete more effectively in an evolving financial landscape.