Getting funding for your business shouldn’t feel like waiting in a long, silent queue with no idea when your turn will come. Yet for many business owners, that is exactly what it feels like. You apply, submit documents, answer questions, and then wait. Sometimes for weeks.

The truth is, approvals do not have to take that long. Some businesses get funded in a matter of days. Others get stuck for months. The difference usually comes down to how well the business is prepared and how clearly it fits what lenders are looking for.

Let’s talk about what actually makes the process faster. Not theory. Not generic advice. The real things that move an application forward.

Lenders Are Not Just Looking at Numbers

A lot of business owners think approval is all about credit score. It is part of the picture, but not the whole thing.

When a lender reviews your application, they are asking a simple question. Can this business pay the money back without stress?

They look at patterns more than promises. Steady revenue matters more than projected growth. Clean records matter more than big claims. If your numbers tell a consistent story, things move faster. If they raise questions, everything slows down.

Cash Flow Speaks Louder Than Anything Else

If there is one thing that can speed up approval, it is strong cash flow.

You might have a decent credit score and still get delayed if your cash flow looks uneven. On the other hand, a business with average credit but steady income often gets approved faster.

Lenders go through your bank statements carefully. They notice patterns. Regular deposits are a good sign. Sudden drops or frequent overdrafts are not.

Some simple habits help more than people expect. Keeping expenses predictable. Avoiding unnecessary withdrawals. Making sure your account activity looks stable month after month. These are small things, but they build trust quickly.

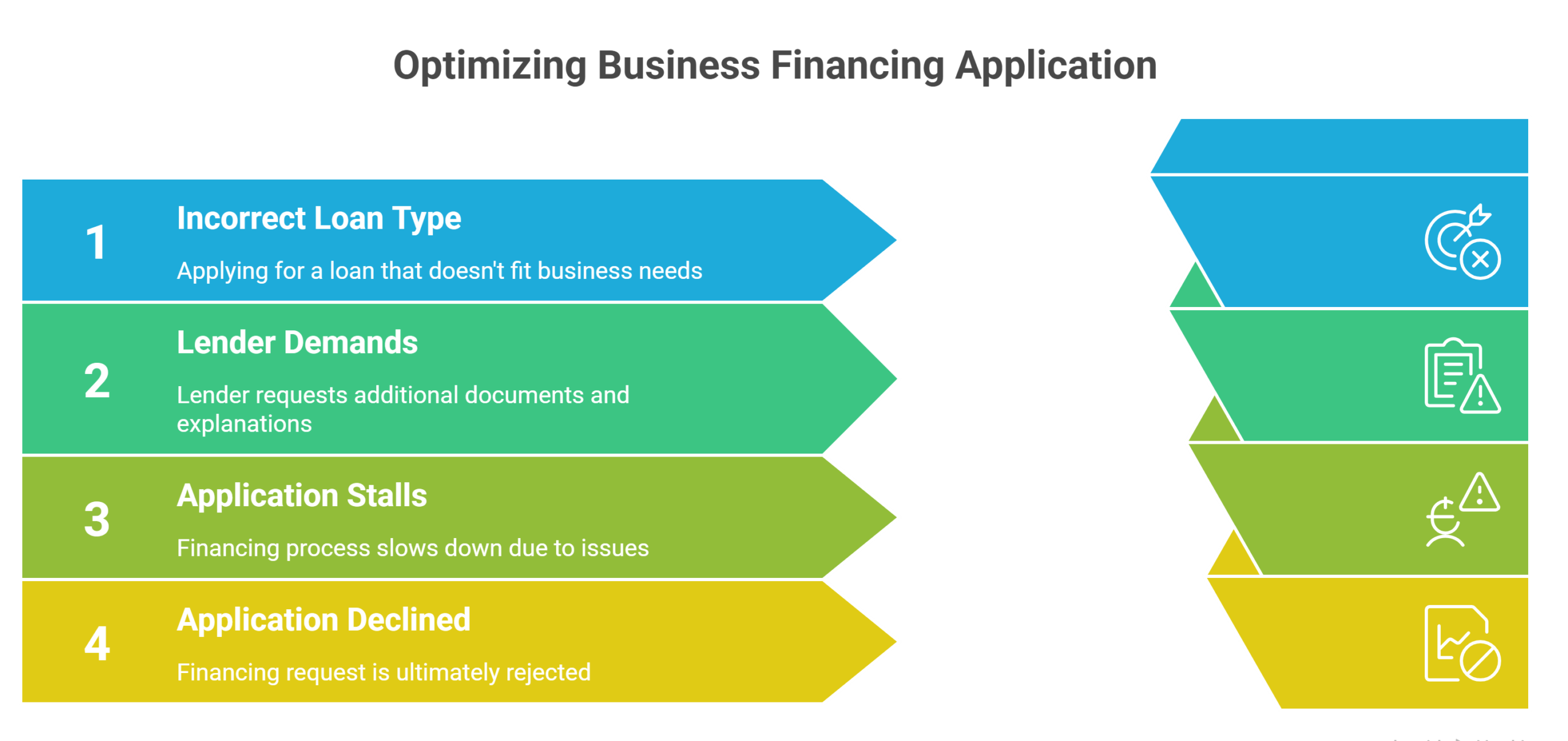

Applying for the Right Type of Financing Matters More Than You Think

This is where many businesses lose time without realizing it.

They apply for a product that does not fit their situation. Then the lender asks for more documents, more explanations, more time. Eventually the application stalls or gets declined.

For example, businesses with physical assets often move faster with abl financing. Since the funding is backed by assets, the lender spends less time worrying about risk. That alone can shorten the approval window.

The key is simple. Do not chase a loan type just because it sounds popular. Choose the one that fits how your business actually operates.

Your Invoices Can Work for You

If your business sends invoices and waits 30 or 60 days to get paid, you already know how frustrating that gap can be.

That gap can also slow down your financing approval if your cash flow looks tight on paper.

This is where working with an Accounts Receivable Financing Company in California can make a real difference. Instead of waiting for customers to pay, you unlock that money early. Your cash flow improves almost immediately.

From a lender’s point of view, that changes everything. A business that gets paid faster looks more stable. And stable businesses move through approvals much quicker.

Incomplete Applications Are the Biggest Time Killer

This one sounds obvious, but it happens all the time.

A missing bank statement. An outdated financial report. Numbers that do not match across documents. These small gaps create delays that could have been avoided.

Lenders do not move forward until everything lines up. If they have to come back and ask for more details, your application goes to the side while they wait.

It helps to treat your application like something you would present to an investor. Clean, organized, easy to follow. When everything is in place from the start, decisions happen faster.

Credit Still Plays a Role, Just Not the Only One

Even though cash flow carries a lot of weight, credit has not disappeared from the equation.

A history of late payments or high debt can raise concerns. It does not always lead to rejection, but it can slow things down. The lender may take extra time reviewing your file or ask for more supporting details.

Improving your credit profile is not always a quick fix, but even small improvements help. Paying down balances, staying current on obligations, and avoiding new debt before applying can make your application look cleaner.

The Lender You Choose Can Speed Things Up or Slow You Down

Not all lenders operate the same way.

Some move cautiously. They take their time, review every detail, and follow strict guidelines. Others are built for speed. They rely more on real time data and faster decision models.

If timing matters, you need to be selective.

Working with a lender who understands your industry also helps. They already know what typical numbers look like. That reduces back and forth questions and speeds up the process.

Stability Makes Decisions Easier

Think about it from the lender’s perspective. A business that looks steady is easier to approve.

If your revenue has been consistent for the past year or two, that works in your favor. If your customer base is spread out instead of relying on one or two clients, that helps too.

Even small details matter. A business that has been operating for a few years feels less risky than one that just started. That sense of stability often leads to quicker approvals.

Asking for Too Much Can Slow Everything Down

It is tempting to ask for more funding than you actually need. Just to have a cushion.

But lenders look closely at whether your business can realistically handle the amount you are requesting. If it seems too high, they take a deeper look. That adds time.

In some cases, they may come back with a lower offer anyway.

It is better to ask for a number that clearly fits your financials. It shows discipline and makes the decision easier on their side.

Relationships Still Matter in Lending

This part often gets ignored.

If you only talk to lenders when you urgently need money, you are starting from zero every time. No history, no familiarity, no trust.

On the other hand, businesses that build relationships early tend to move faster when they apply. The lender already knows how they operate. There is less uncertainty.

Even a simple conversation before applying can give you insight into what the lender expects. That alone can save time later.

Alternative Financing Has Changed the Game

The financing world has shifted a lot in recent years.

Traditional loans are no longer the only option. Many businesses now choose faster, more flexible solutions that focus on performance instead of rigid requirements.

A Business loan USA provider that works with real time data can often approve applications much faster than a traditional institution. Less paperwork. Fewer delays. More focus on what your business is doing right now.

For businesses that need quick access to capital, this flexibility can make a big difference.

Mistakes That Quietly Delay Approvals

Some delays are not obvious. They happen in the background.

Submitting numbers that do not match across documents. Applying to too many lenders at once. Waiting until cash flow becomes a problem before applying.

These things create hesitation on the lender’s side. And hesitation slows everything down.

Keeping your financials clean and your approach focused helps avoid these issues.

What It Really Comes Down To

There is no single trick that guarantees fast approval. It is a combination of things working together.

Strong cash flow. The right financing choice. Clean documentation. A realistic request.

When these pieces are in place, the process feels very different. Less friction. Fewer questions. Faster decisions.

Final Thought

Getting approved faster is not about rushing the process. It is about removing the reasons for delay.

When your business looks clear, stable, and prepared, lenders do not need to pause and second guess. They move forward.

And that is really the difference. Not luck. Not timing. Just a business that is ready when the opportunity comes.